Money Markets - July 2024

Moderating inflation, election risks.

“In the truest sense, freedom cannot be bestowed; it must be achieved.” —Franklin D. Roosevelt

Welcome to AlphaPicks’ monthly market update - a rundown of global markets for the coming weeks in under ten minutes.

This month, our guest contributor is:

Here’s what you need to know…

Macro

June provided us with a continued theme of moderating inflation and monetary policy reacting to this.

In the developed markets, we got two central banks that started their cutting cycle. This included Canada, with the BoC reducing its interest rate by a quarter-point to 4.75%, marking its first rate cut in four years.

Similarly, the ECB cut the benchmark rate by 25bps at the June meeting. Later in the month, the Swiss National Bank provided us with a second 25bps cut, taking the base rate down to 1.25%.

This theme is picking up pace, with the US and UK also on alert for the first rate cut in the early autumn. The macro driver for this continues to be inflation returning towards target levels for most major nations. Many still have a robust labour market, so the cuts are seen as coming from a position of strength. Even though wage pressures are a key risk in this dynamic for July and beyond, the market perception of cutting from a strong base means that equity markets should continue to be supported.

Below we show the change in inflation versus the same reading a year back. The broad trend of moving back to the 1.50-3.50% region has certainly provided some cautious optimism to take into the month ahead.

The other theme that drove markets was election results. Throughout June we covered this in detail, noting divergence from the expected poll results in South Africa, Mexico and India.

In India, Modi and the BJP coalition secured 292 out of 543 seats in the Lok Sabha, with the BJP alone winning 240 seats, falling short of an outright majority. This marked a decrease from their previous performance (e.g in the 2019 election mentioned above).

Modi thus had to spend rushed time trying to secure a working Government, but naturally the demand of the smaller parties meant that negotiations in order to get support were tough.

As a friendly reminder, you can become a premium subscriber with us for just £10 a month. This provides you full access to our weekly articles without a paywall, including our flagship Monday trade ideas and access to what we are buying and selling in our Global Asset Portfolio.

In South Africa, the ruling African National Congress (ANC) failed to secure a majority for the first time since the end of apartheid, receiving just over 40% of the vote. This marks a dramatic decline from its previous dominance, meaning that just like India, a coalition was needed.

Investors cheered an agreement between rival political parties to back the re-election of Cyril Ramaphosa as president. This agreement paves the way for a broad government coalition led by the African National Congress and the business-friendly Democratic Alliance.

We covered the implications for South African assets in particular here:

A Cape Of Good Hope

Emerging markets have offered many opportunities in recent months. Javier Milei’s election to President in November saw an economic turnaround in Argentina, driving its stock index (MERVAL) up 150% since. With the India elections done and dusted, the Sensex is back at ATHs and driving higher. Now, we have South African markets rallying, along with the SA Rand.

While you can read the broader run down of early June elections here:

Trading A Wild Week Of Elections

This week has been a rather crazy one for EM markets with some rather unexpected results in national elections. As the respective markets still try and digest what the results mean for the governing parties going forward, we feel there’s some opportunities to be had in this space.

The macro calendar for July has various events which we are watching closely. To begin with, the first round of the French elections is today (30th June), with the second round taking place the following weekend.

The other election that we are watching for is here in the UK, which is on Thursday 4th July.

The next Fed meeting is right at the end of the month (Wed 31st July), where there’s a slim 10% chance of a rate cut. The ECB meet on Thurs 18th July, whereas the Bank of England take a break and meet again in August.

Equities

Although the broad macro theme played out throughout May, this didn’t always correlate through to respective equity markets.

The best case of the correlation came from the US, where a lower than expected inflation print and a neutral Fed allowed stock to continue their march higher. AI and semiconductors led the charge in the risk-on mood.

Elsewhere things were more nuanced. Election results mentioned earlier saw idiosyncratic moves higher in South African equities, while the snap election call saw the French CAC 40 tumble lower.

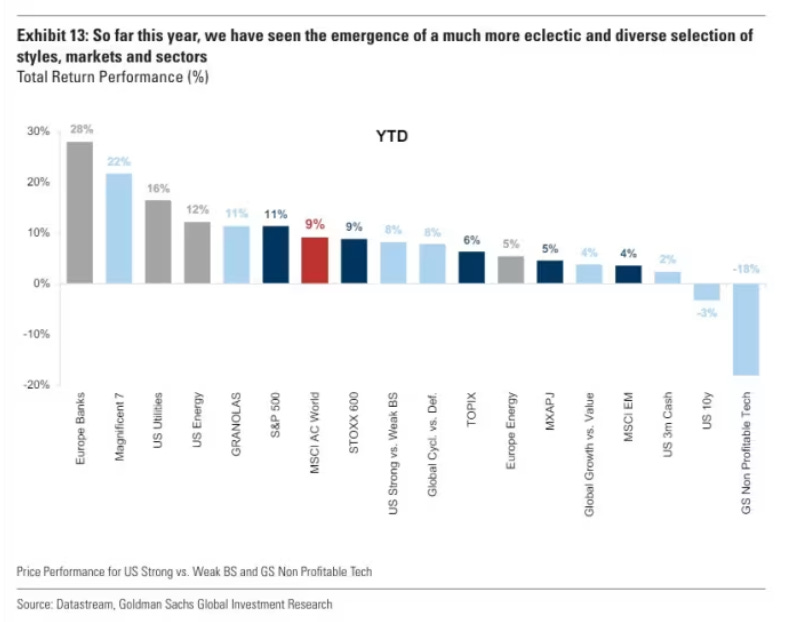

One of our favourite charts from May came from Goldman Sachs, who pointed out that equity returns this year aren’t simply coming from owning the MAG7, but rather from a much more diverse selection of sectors and markets:

We don’t want to give away too much from our Global Asset Portfolio review which drops next Wednesday. However, during the month we did add exposure to UK equities in particular. We continue to see good value in large and mid cap names, and it appears we aren’t the only ones.

M&A activity in the UK market has really picked so far this year. One notable acquisition is the purchase of Barratt Developments by Redrow for £3.2bn. We’re also in the middle of Hargreaves Lansdown getting bought out for £5.4bn by a private equity consortium, alongside other smaller deals.

One particular case that we have a position in heading into July is Britvic. Carlsberg has made two takeover bids for Britvic over the past month. These were both unsolicited, but highlights its strategic interest in expanding its presence in the soft drinks market.

The initial bid, valued at £800 million, equated to 1,200p per share in an all cash offer.

Britvic initially rejected the offer, believing it undervalued the company’s growth potential and market position. In response, Carlsberg tabled a second, higher bid of £850 million, which equated to 1,250p per share. Even though this was around a 20% premium to the share price close on that day, the offer was turned down.

We bought the stock for our portfolio at 1,080p and will either will take profit at 1,300p based on a future offer that may/may not come. If this does happen, it’ll bank us good profit in a short space of time (a few weeks).

Given the share price jump on the offer rejection, if Carlsberg walk away we don’t see downside risk. Rather, we think organic growth will support a move towards 1,300p anyway, albeit over the course of the next year or so.

Looking ahead at July, we don’t really see many warning signs that should derail the broader equity market rally.

In the US, we continue to believe that tech and related sectors outperform, with the NASDAQ 100 likely offering the highest returns.

What we’re watching in the short term is how strongly dip buyers emerge on Nvidia. The sharp three day correction lower has been bought so far, and we expect that any move lower will be stopped around the $112 level:

FX

Guest Contributor: Arno Venter

What is up with the Pound?

The British Pound has been on an absolute tear this year. Recent developments in data and sentiment suggest that Sterling’s strength might be challenged in the next few weeks.

At the start of the year a lot of the outperformance was associated with monetary policy where the BoE was seen as one of the outliers to keep rates higher for much longer than their peers.

However, the shifts in money market expectations over the last two months have eroded that view.

As we can see from the table above, the expected amount of cuts expected for the BoE is not a reason for Pound strength anymore. The intriguing thing is that the Pound has not responded to the market’s changes in rate expectations over the past few weeks.

By using a normalized real effective exchange rate comp, we can start to appreciate just how strong Sterling has been relative to its peers. The reason why this is important is because it’s easy to blame much higher inflation for a lot of the strength, but stripping that out as a variable still leaves Sterling on the top of the pile.

Furthermore, inflation in the UK is not the same problem it was for the BoE just a few short months ago. Apart from wages and Services inflation which has remained stubborn, headline and core CPI (which policy decisions should be based on) has seen decent deceleration.

For the BoE, their most recent meeting saw interesting language used in their voting split explanations which suggested that votes between holding rates and cutting rates very finely balanced.

That’s basically the BoE’s way of telling us that if it wasn’t for the upcoming election there’s a likelihood that they could have cut rates at that meeting. But whether they admit it or not, politics matter when they make decisions.

When it comes to growth and the labour market, we’ve seen clear signs of deterioration in the labour market, which suggest that wages should start to moderate as the labour market continues to slow.

On the growth side, looking at a normalized comp of the Citi Economic Surprise Index, there is reason to believe it’ll be tough for data to surprise higher in the weeks and months ahead, given the herding mentality and recency bias in forecasting from the economist community.

Keep in mind that growth does not need to collapse to be seen as negative. If analysts and economists use recency bias to estimate data too lofty, and actual data surprises lower as a result, that will still be seen as a negative for Sterling.

The latest flash Services PMI saw a big surprise miss, and since it makes up over 80% of UK GDP it is something that should have mattered to Sterling.

On the political side, looking at a chart of the 1-month risk reversals for GBPUSD, it seems like the market is not pricing in any meaningful risk premium for the upcoming election. Given the polling data one would have assumed a bit more risk associated with the potential uncertainty, regardless of outcomes.

So, here is where we stand:

- We have a market that no longer prices any meaningful rate differential for the BoE versus its peers.

- Sentiment that suggests a cut would have been possible had it not been for the election.

- A moderating labour market, decelerating inflation and higher risk of growth data surprising lower.

- A currency that trades much stronger than its peers on both a relative and absolute basis (looking at geometric and REER strength).

- Almost no risk premiums priced for upcoming election risks, which almost seems irresponsible for those that would at a minimum want to hedge some currency risk.

- Risk to reward favours downside far more than chasing more upside at this stage.

With all of the above in mind, it would seem that the path of least resistance is tilted lower for Sterling from its current levels, and that further gains will be much harder to come by compared to previous upside seen earlier this year.

My base assumption would be that once the election is out of the way, attention should zero in on the data and the BoE, and on that front, I think the bias is titled lower.

With so many idiosyncratic risks in play right now, I prefer expressing this view against a basket of currencies instead of having all the eggs in one basket. It’s going to be an interesting next few weeks for the Pound.

AlphaPicks:

The US Dollar Index (DXY) finished the month higher than where it started. Bulls were cheered on by the hawkish tilt in the Fed’s new dot plots, as well as being buoyed by decent US data prints.