Money Markets - March 2024

Rate cuts, recessions and rising equities.

“What we wish, we readily believe, and what we ourselves think, we imagine others think also.”

- Julius Caesar

Welcome to AlphaPicks' monthly market update - a rundown of global markets for the coming weeks in under ten minutes.

Here’s what you need to know…

Macro

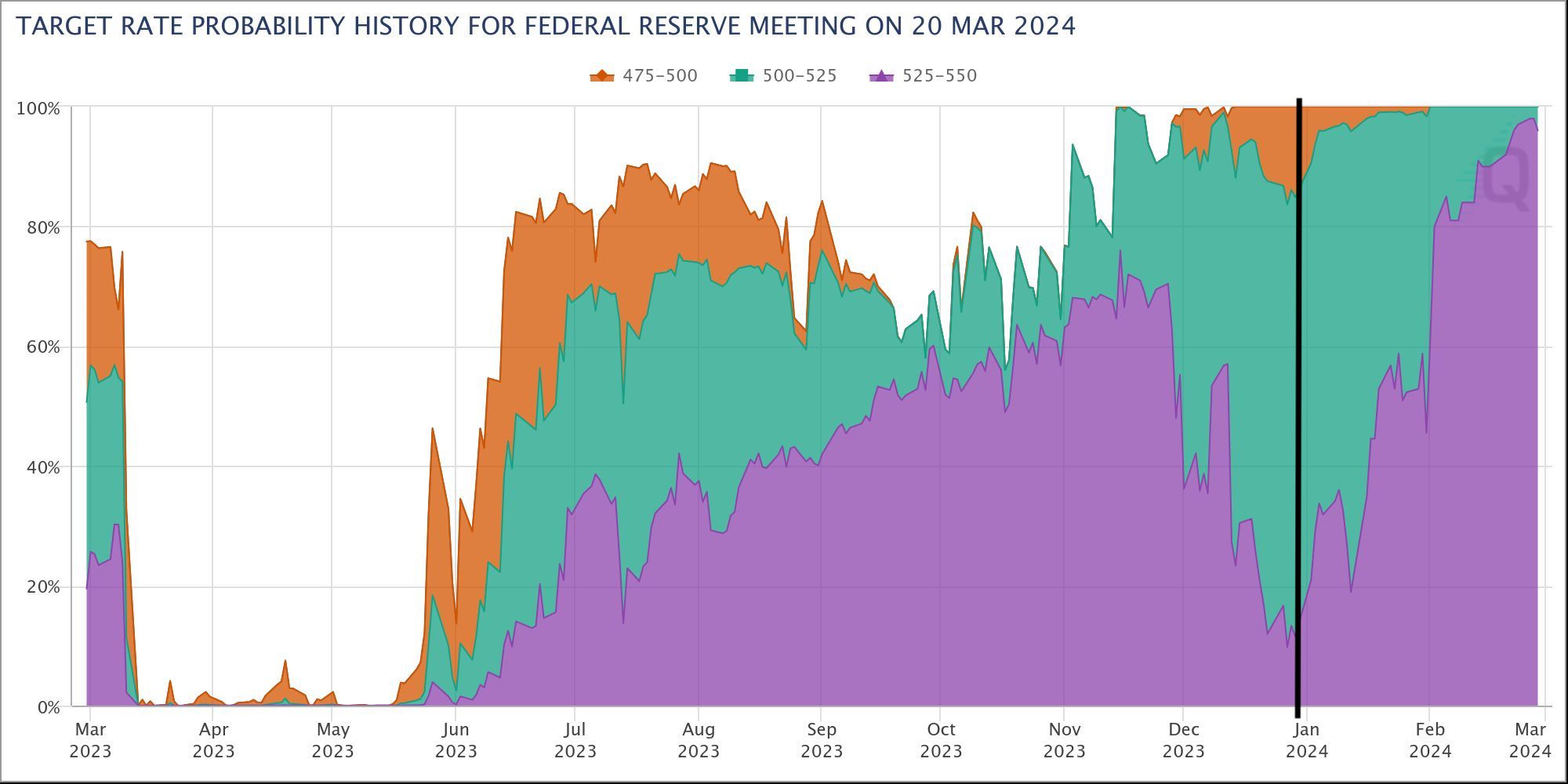

The first topic of conversation is the FOMC March meeting. Going into 2024, this meeting was teed up to be the first-rate cut that markets would see in this cycle. As of the last trading day of 2023, there was a 73.35% probability of one rate cut in March and 15.11% for two quarter-point cuts.

That narrative has changed dramatically, with markets now expecting just three cuts in 2024, much more in line with the Fed’s dot-plot. Fed speakers continue to remind market participants that they are data-dependent and not calendar-dependent.

PCE data was keeping markets on the sideline. The data release avoided any surprises, so now we can wait patiently to hear the Fed rhetoric at the end of the month.

Lowering interest rates prematurely would be a worse mistake for the European Central Bank than reducing them too late. The euro-zone inflation rate dropped to 2.6% last month, missing the economist's prediction of a slowdown to 2.5%. That supports ECB officials who don’t want to rush into lowering borrowing costs. Cutting too quickly and losing control of inflation poses a real challenge for the bank.

Financial markets began the year expecting the first Bank of England rate cut in May. That’s since been pushed back to August. That’s partly because of the prospect of tax cuts at the March 6th spring budget. All else equal, that would require slightly tighter monetary policy, though in practice the room available for sizeable tax cuts appears pretty limited, barring some major fiscal gymnastics.

The BoE will want to see the April and May inflation figures, the latter of which is released the day before the June policy meeting. So, as far as a March outlook, there is unlikely to be too much of a sentiment change.

Indices

US indices have stubbornly risen higher throughout the year. The AI theme can keep things going (or propped up) in the US. Avoiding the final hurdle of PCE ended last month on a “no news of bad news” theme.

While markets delayed the rate cut story till later in the year, they haven’t let that change the bullish sentiment. Earnings season comes to an end with no major surprises or effects on the greater market.

Euro markets have been helped higher by the success of ‘Granolas’. You can read more about this group here. UK markets have remained fairly unchanged YTD and also through Feb, finishing the month just 0.7% higher.

The rangebound FTSE is still yet to make a new all-time high, unlike its peers in Europe and the US. Things are likely to be the same in the near future.

Europe markets can continue higher, offering some opportunities to go long on an index and single-name point of view.

In 1989, the Japanese Nikkei 225 index reached an all-time high of 38,915.87, which was accompanied by great excitement. However, the following 34 years were marked by numerous crises, natural disasters, deflation, and a decline of almost 80% in the index. Last week, markets were able to rejoice as the Nikkei finally recovered its 1989 level, reaching 39,239. This recovery has been driven by the global semiconductor stock boom, along with other more fundamental factors.

China is another story, but one that could be changing tune. After declining for the last few years, investor interest in a contrarian bet is rising as the markets hold some recent gains. Chinese Premier Li Qiang said ‘effective measures’ were needed to boost confidence.

We think the start of this recovery will continue, but we are staying on the sidelines with this market as we believe there are better opportunities for capital deployment in other markets.

Commodities

Oil is slowly but surely making its way higher. We are yet to tap the $80 mark on US crude, but speculation that OPEC+ will extend supply cuts and the market will gradually tighten could take us there in the month.

We are starting to see some signs of life in global manufacturing, petrochemicals and strong fuel demand in Asia.

Gold is lining up to be a strong performer. PCE data leading the USD lower helped the precious metal start its next move higher, with Friday's price action leading to the highest weekly close on record. Fast incoming is the fatal 2070-2100 level that has kept the commodity withheld for some time now.

This is a main watch for us, as well as related names, such as gold miners.

Currencies

In FX, March promises to be a busy month. Given the sensitivity to macro drivers, the US Fed, BoE, ECB, BoJ and other key central bank meetings will be closely watched.

The latest round of CPI readings and labour reports are another added layer that will provide traders with a finger on the pulse of each country’s respective health.

In terms of specific pairs we’re watching for March, we start with USDJPY. As we close out February, we had interesting comments out from the BoJ’s board member Hajime Takata. He commented that the central bank's price target is finally coming into sight. This boosts expectations that an exit from the current policy stance will be seen shortly.

USDJPY fell circa 0.5% on the comments, out of the 150-152 range dubbed ‘intervention territory’. March will be a key month, either for a break lower (based on a weaker USD / stronger JPY) or for this to be another dip that gets bought by the market to test 152 again.

The other pair for the month ahead is EURNZD. We saw the Kiwi Dollar weaken sharply on Wednesday following the central bank Governor walking back on comments that another interest hike is needed.

Despite this knee-jerk move, we think traders will look to buy the dip in NZD pairs into March. They are still the most hawkish G10 central bank in our view (excluding the BoJ… but would you call them hawkish?), and so when you pair it off against somewhere like the Eurozone, where the ECB really need to start cutting in the spring, we feel EURNZD is one to watch for a move lower in March.

Crypto

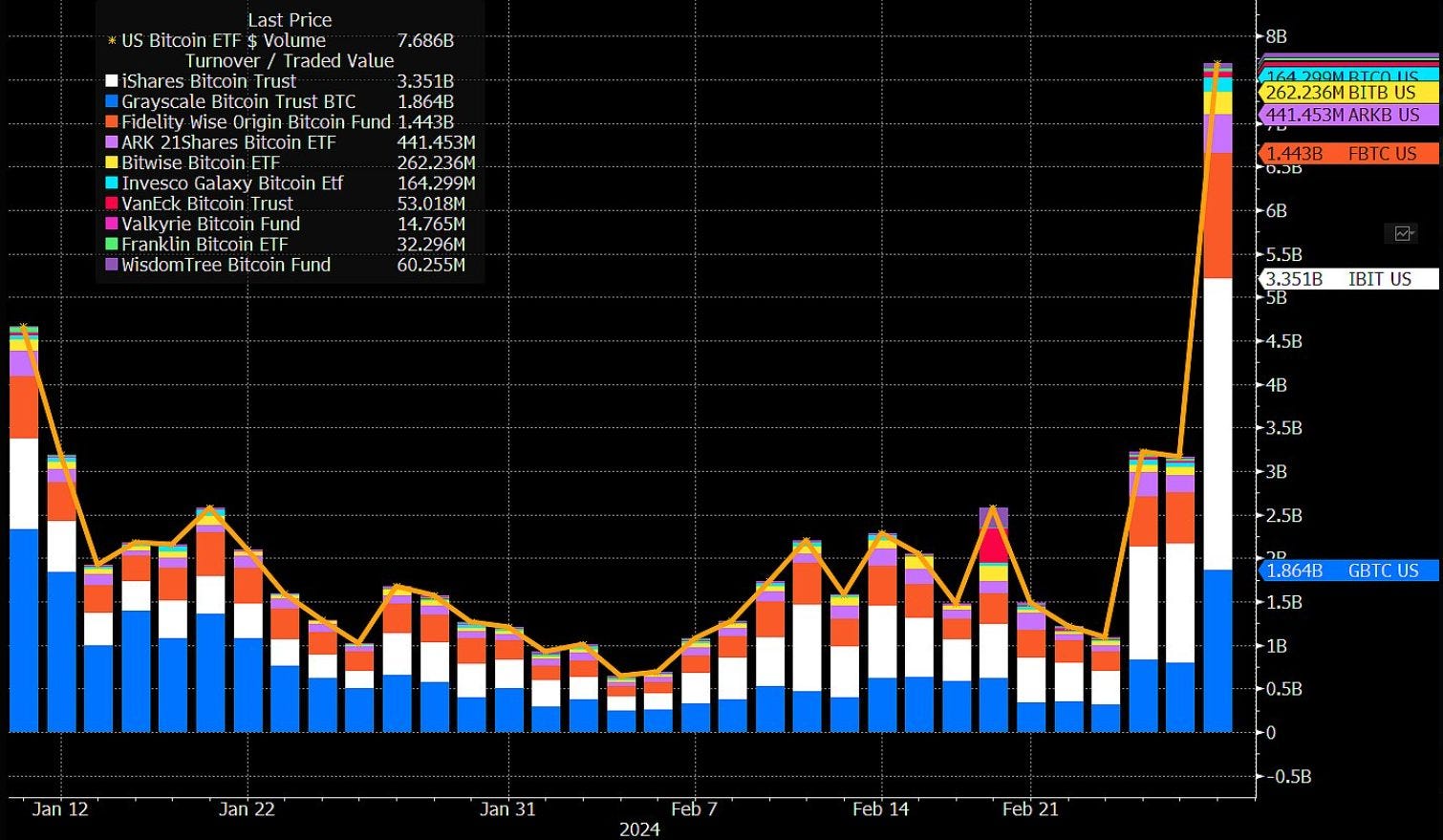

The crypto market has been recovering for some time now. But last week, we think it’s fair to say that the mania is well and truly back. Bitcoin is flying, random dog tokens are gaining 30 or 40 per cent every few days, and Coinbase is crashing. It all feels back to normal.

Bitcoin ETFs had their highest inflow since launch, with the underlying asset up more than 30% since. What next? New high in March?

Bitcoin’s ATH of $69,000 is well within reach as the price surges to $64,000. The closely-watched ‘halving’ event will be a topic of discussion in April’s ‘Month Ahead’.

Bitcoin has outperformed traditional assets like stocks and gold in 2024, providing a locus of volatility for traders seeking opportunities. We expect much of the same as mania builds: volatile price, outperformance, and the feeling of “I wish I’d bought more” from the masses.

A question to leave you with: Tell us the difference between BTC and TQQQ?

“Soros has taught me that when you have tremendous conviction on a trade, you have to go for the jugular. It takes courage to be a pig. It takes courage to ride a profit with huge leverage.”

- Stanley Druckenmiller

Like the content guys

Big!