Operation Twist

Japan's bond market is no longer the anchor. It's the shockwave.

For years, Japan’s bond market was a place where volatility went to die. Traders could safely ignore Tokyo until New York closed, and sometimes even after. Under the Bank of Japan’s yield curve control (YCC) policy, introduced in 2016, JGBs were domesticated and tranquilised. The 10-year yield was pinned near zero, and activity was so subdued that benchmark bonds could go days without trading. The BOJ absorbed wave after wave of supply, turning its sovereign market into a controlled experiment in modern monetary theory.

That era is over.

Since 2022, the BOJ has been unwinding its grip on the curve. First by loosening the YCC band, then scrapping it altogether, and now by slowly tapering its bond purchases in what amounts to a belated and disorderly normalisation. The consequences have been swift. Japanese yields have surged, auctions have faltered, and volatility has spiked to levels not seen in decades. What was once a sleepy corner of the global fixed income market is now one of its main sources of risk.

From Anchor to Epicentre

The shift in Tokyo has not stayed in Tokyo. As Japan dismantles its monetary firewall, the global bond market feels the aftershocks.

Super-long JGB yields (30- and 40-year maturities) have been leading the charge higher. When a recent 20-year auction bombed, it sent ripples through duration markets worldwide. That same day, US 30-year Treasuries hit a 19-month high and German bunds followed. The correlation between Japan’s 30-year yields and those of the UK and US has hit record levels.

The reasons are structural. Japan is the world’s largest creditor, with deep holdings in overseas debt. Japanese investors have long been key players in the US Treasury and European sovereign markets. But as yields rise at home and hedging costs fluctuate, the relative appeal of foreign bonds declines, prompting selling abroad and volatility everywhere.

Moreover, the BOJ’s unwind is forcing a reallocation across benchmarks. Japanese government bonds account for 16.7% of the Bloomberg Global Treasury Total Return Index, second only to the US. When JGBs drop, global bond funds take the hit. Passive flows become forced sellers. Diversification becomes a liability.

This is the new reality. Instead of stabilising global yields, Japan is now amplifying them. Where once Tokyo’s 9 a.m. open was a footnote, it is now the first act in a daily bond market drama that spans continents.

Volatility by Design

Ironically, the recent disorder stems from a BOJ attempting to restore order. In theory, winding down a decade of QE and YCC should improve liquidity and price discovery. In practice, the exit from repression has triggered fresh distortions.

The pressure shows at the long end, but the BOJ tapering has prioritised the short end. The result is a fragile, underbid super-long sector.

The May 40-year auction saw the weakest demand in almost a year. A 20-year offering earlier in the month posted the lowest bid-to-cover for over a decade, a data point that carries echoes of another inflationary regime. Traders are already shifting duration risk back to the BOJ in its rinban operations, showing a clear preference for offloading short-term paper while avoiding longer maturities.

This tension has revived speculation of a modern-day Operation Twist, a deliberate skew in debt issuance from the long end to the short end. Market chatter is growing, and the Ministry of Finance is under pressure. Their meeting with primary dealers later this week will be a focal point.

The Ueda Pivot

The BOJ didn’t hike, but it did blink.

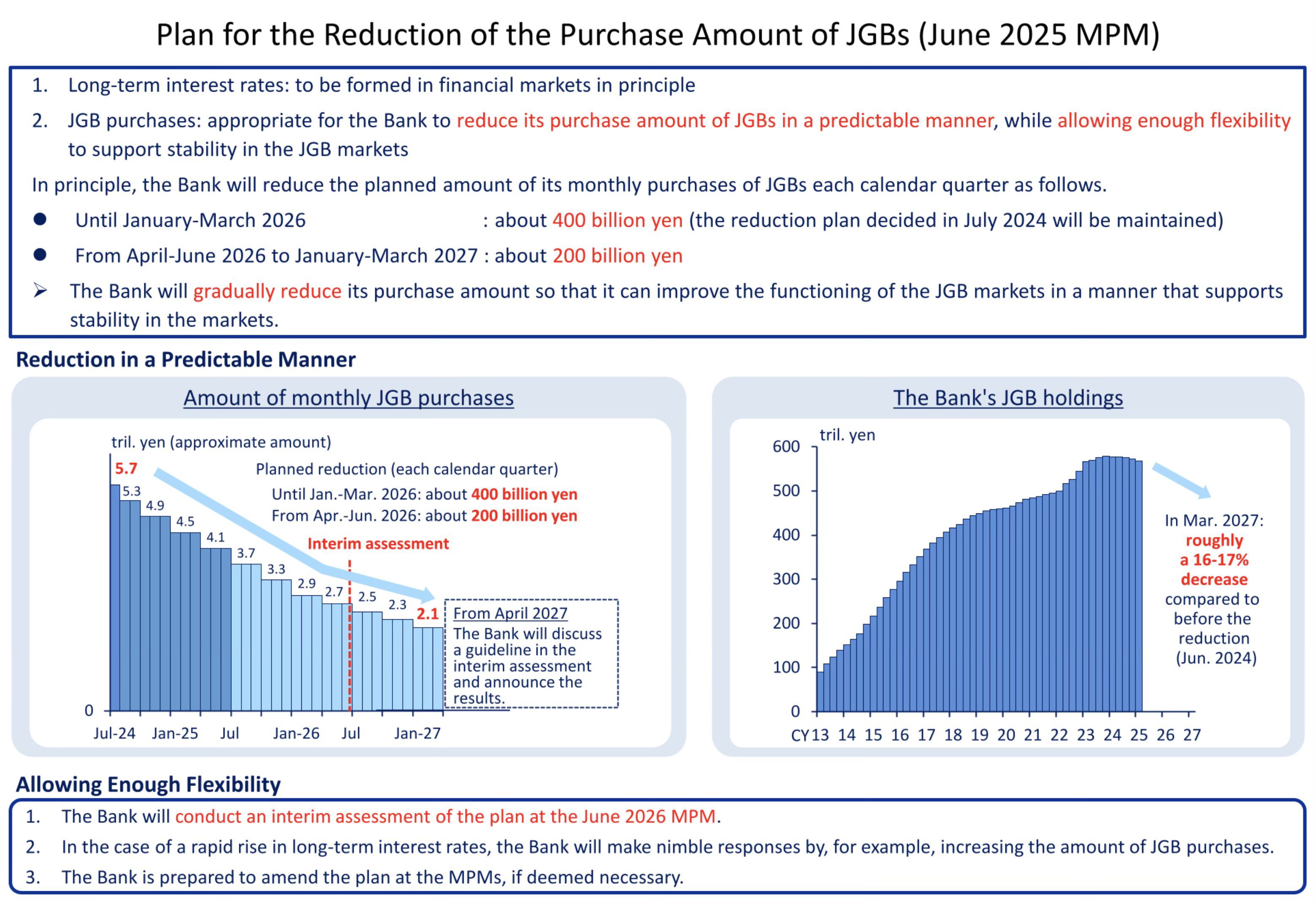

At this week’s policy meeting, Governor Kazuo Ueda left the short rate unchanged at 0.5%. But beneath the surface, the BOJ recalibrated. Starting next fiscal year, the central bank will halve the pace of its quarterly bond purchase reductions from ¥400bn to ¥200bn—a modest shift, but a clear nod to growing dysfunction in the long-end and weak auction outcomes.

Ueda’s press conference was a masterclass in central bank understatement. No forward guidance. No firm timing on rate hikes. Just enough to keep July optionality alive, especially as sticky inflation and higher energy prices cloud the horizon. The yen barely reacted. Yields nudged higher. But the subtext was clear: the BOJ is still on a tightening path, just cautiously.

Underneath the messaging, structural changes are afoot. The BOJ also adjusted its bond-lending operations, expanding the pool of securities eligible for loans. That means more notes in circulation and less deadweight on the BOJ’s balance sheet. Simultaneously, the frequency of purchases in the 1- to 10-year sector will fall from four times a month to three, even as the headline taper slows.

These are small moves. But they carry a big message: the BOJ wants a functioning market. One with a two-way flow, where auction risk matters and price isn’t a foregone conclusion.

The era of anaesthetised Japanese bonds is over. The training wheels are off.