The S&P 500 extended its winning streak to a fourth consecutive week, though the path higher continues to look more conditional than convincing. Price action through the week was defined by the same pattern that has dominated recent months: early optimism tied to ceasefire dynamics giving way to midweek uncertainty, before a late rally (although this time was driven by a combination of AI momentum and incremental geopolitical hope).

Technology, as is often the case, again did the heavy lifting. At this stage, the equity market is a continuation of the “chips as macro” regime, where incremental demand signals from AI infrastructure drive index-level performance.

Elsewhere, the rotation out of defensives was notable. Healthcare lagged amid a combination of weak earnings and softer prescription data, with pressure on weight-loss drug narratives feeding through to the broader pharma complex. Financials also underperformed, weighed down by disappointing results and a lack of clear participation in the broader rally. The divergence highlights a market that is still selective, rewarding growth visibility while penalising anything that hints at cyclical or structural fragility.

Macro remains in a holding pattern. The absence of major data or Fed communication ahead of the blackout period has left markets trading predominantly on geopolitical headlines and earnings anticipation. Strong retail sales provided a reminder that the US consumer remains intact for now, but the broader picture has not shifted materially. Policy expectations are largely unchanged, and the market continues to operate within a narrow band of outcomes: resilient growth, sticky but manageable inflation, and a Fed that remains on hold unless forced to act.

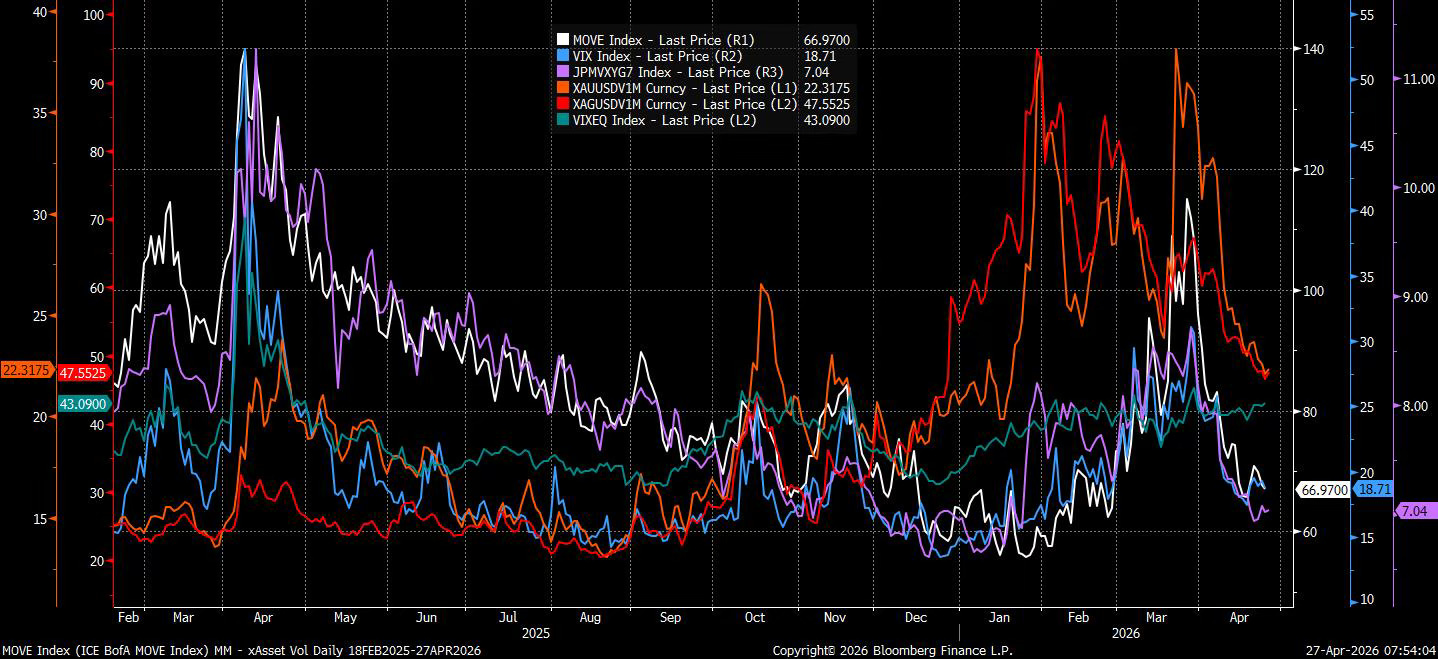

Across assets, volatility continues to compress. FX markets were notably subdued relative to recent weeks, with the dollar trading in line with incremental Iran-related developments rather than leading them. Risk reversals point to a market that is tactically long USD on geopolitical uncertainty but structurally biased toward weakness over a longer horizon.

In rates, the move higher in yields, particularly in the 2y–5y, reflects a modest re-pricing of risk rather than a decisive shift in the policy outlook.

The broader takeaway is that equities are grinding higher without a clean macro anchor. The leadership remains narrow and micro-driven, the drivers remain flow-driven, and the geopolitical backdrop continues to inject episodic volatility. As long as the AI capex narrative holds and ceasefire dynamics avoid a renewed escalation, the path of least resistance may still be higher. But the market is increasingly behaving like one that is being pulled upward by momentum.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Micro Is Leading”

“Carry Trade Indication”

“The Reverse ‘Saudi Put’ on Oil”

“A Crypto Stealth Rally”

Micro Is Leading

Macro factors have dominated equity direction in recent weeks. The S&P 500 moved lower in a relatively orderly fashion, as markets priced in war risk and attempted to map the economic spillovers from the Middle East. Positioning played a role here, with little appetite to press shorts. Memory of last April’s squeeze is still fresh.

As tensions between the US and Iran appeared to peak, markets were quick to rebuild length and chase the rebound, helped along by the reassertion of well-worn themes.

Last week marked a shift. Micro factors re-emerged as the primary driver, even if the headline index barely moved. E-mini S&P 500 futures finished the week up just 0.4%, masking a more active underlying tape. The index may look flat on the surface, but beneath it, areas of the market are running hot.

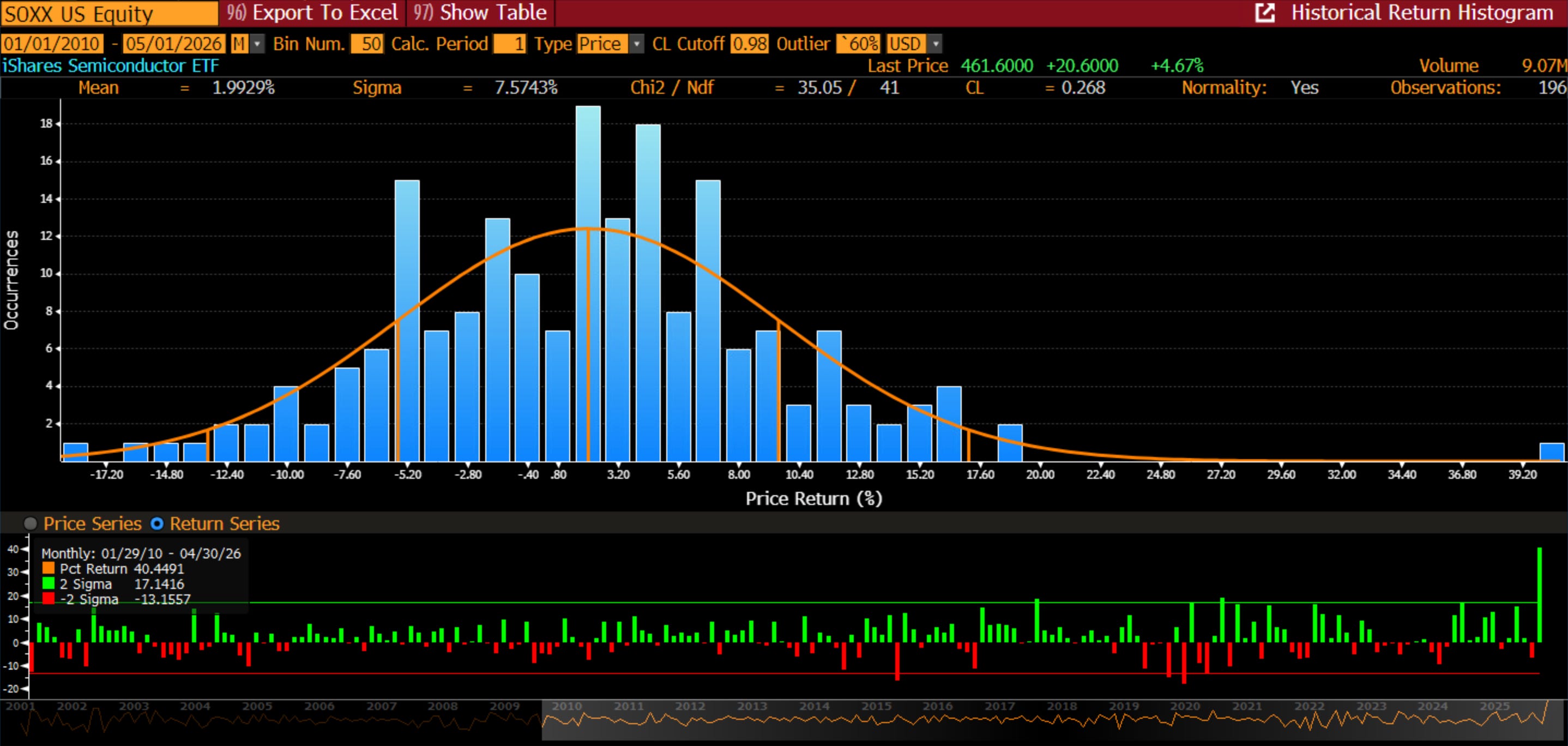

Semiconductors.

April has not yet drawn to a conclusion, but semiconductors are firmly living in the right tail.