Resilient Despite the Pressure

A weekly look at what matters and how to trade it. (May 25th)

Markets aren’t celebrating every part of it, yet the rally lives on.

In what has become a predictable start to these week-ahead notes, US equities extended their winning streak to eight weeks, the longest run since 2023. Improving signals out of US-Iran negotiations helped ease geopolitical risk that has been present in markets since Q1. Oil was lower on the week off due to that same sentiment, but feed-throughs to inflation are already causing problems elsewhere. US rates have pivoted from two cuts priced pre-war to a hike before the year is out. But then again, equities are higher still.

Nvidia (NVDA US) was last week’s main course, but sang a familiar tune of realised coming in below implied vol. We’d call it a non-event compared to NVDA of old. Off 4.5% from prior Friday’s close. As for the results themselves, the flagship of the AI chip trade beat headline expectations, lifted its dividend and announced an $80 billion buyback. The disappointment in price action did not spread across the entire complex (SMH +3.5% on the week), with Dell (DELL US) and Qualcomm (QCOM US) still posting strong gains, but it did reinforce the point that the market is becoming more selective. AI is still the anchor, but not every beat is enough anymore.

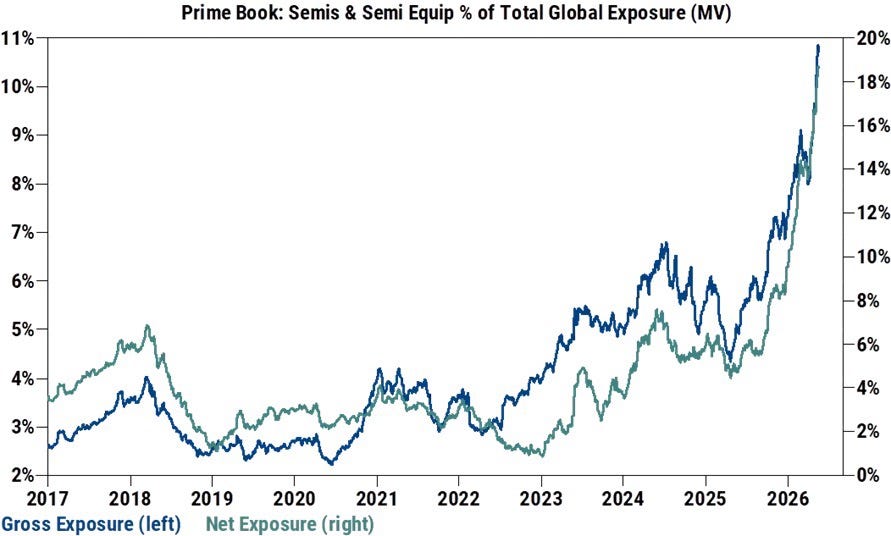

UBS noted that the S&P 500’s recent six-week advance was the narrowest in 35 years, which captures the tension well: the index keeps making progress, but its leadership structure looks fragile. Positioning in semis is quite something.

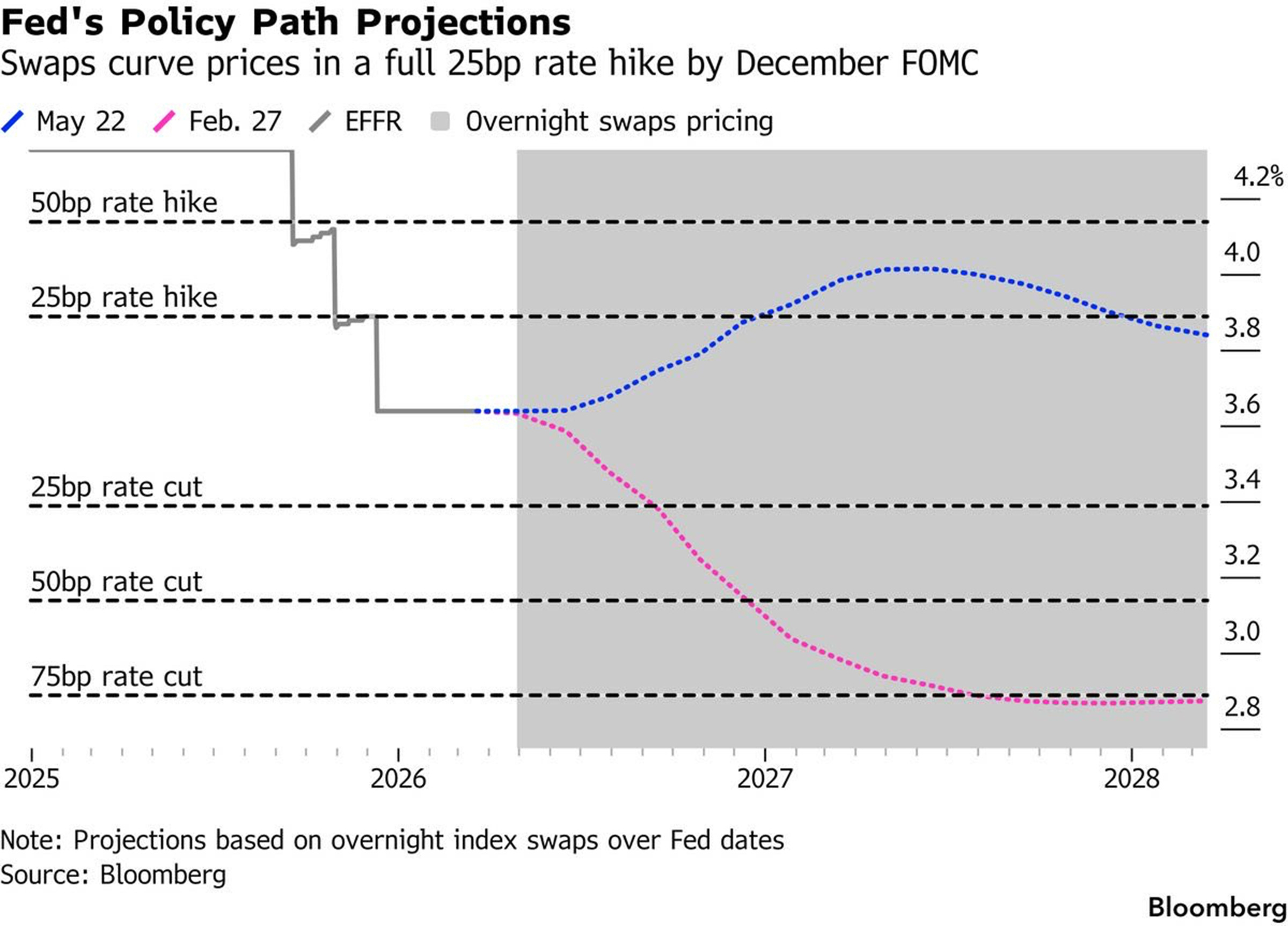

The most important macro development was expressed most cleanly in rates. Waller struck a hawkish tone and backed, removing the easing bias from the FOMC statement, joining other officials who have pushed back against the idea that policy is close to turning easier. The FOMC minutes showed a majority of officials believe a hike could be warranted if inflation persists. Longer-term inflation expectations were revised higher.

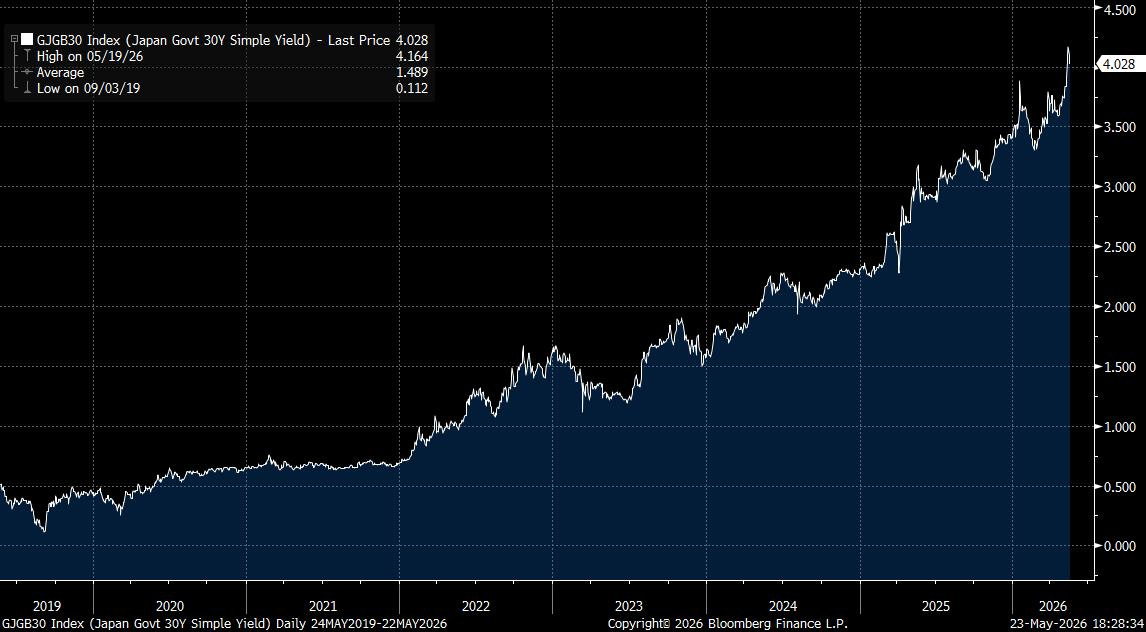

A well-received 20-year auction at 5.122% on Tuesday helped stabilise bond sentiment mid-week. UK 30-year gilts surged toward 6%, and German bund yields also rose, making this a coordinated global bond selloff, not a US-specific story (market memo: “Making Sense of Yields”). Japan’s 30-year exceeded 4%, quite the move from near-zero yields just six years ago.

In currency land, the dollar remained steady, with dips on positive Middle East headlines being bought, suggesting underlying demand remains intact. The dollar bid is increasingly tied to Fed repricing and energy dynamics rather than safe-haven demand.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Rates: Cuts Are Buried, But Hikes Look Too Certain”

“Equities: Shrugging Off Yields, China’s Chips, and WHAM”

“Commodities: Returning to an Old Favourtie”

Rates: Cuts Are Buried, But Hikes Look Too Certain

Kevin Warsh was sworn in last week, but not into the environment markets once imagined when his name first moved into serious contention.

The original Warsh trade was straightforward. A Trump-aligned Fed governor with a public record of criticising the Fed for keeping policy too tight and with a more optimistic view on AI-driven productivity… it all looked like a clear dovish impulse.

That was then.