Sifting Through Small Caps

…and thoughts on central bank rate cycle situations.

While I sit here writing some thoughts on small caps and the regional bank sector, I couldn’t help but be bugged by not mentioning the elephant in the room (the room being the current week and the elephant being the triad of central bank meetings we have lined up).

Right now, at 11 a.m. on a Wednesday morning in sunny London, we’re seven hours into a 32-hour period during which the BoJ, the Fed, and the BoE all announce their interest rate decisions. The build-up to these meetings sees a possibility that each central bank may take a different direction.

The events have already kicked off in Japan. The BoJ raised interest rates to 0.25% from 0-0.1% and unveiled a detailed plan to slow its massive bond-buying, taking another step towards phasing out a decade of massive stimulus.

The size of the move was fairly unexpected, as was the timing of when the announcement would come out. If you have ever worked in FX, you understand.

The Fed are up next. Their path, for now, seems fairly clear: Signal today that rate cuts will likely be coming in the September meeting.

There is, in our opinion, no chance that the Fed cut in today’s meeting with markets completely off guard to that move, and interest rate traders have a September cut priced at 89.6%.

The BoE will take the stage tomorrow. The outcome looks 50:50.

The case for a rate cut is that core inflation measures show a more encouraging trend, aligning with BoE forecasts at 5.1%. Labour market cooling suggests diminishing wage pressures.

The case for holding rates is backed by services inflation stood at 5.7% in June, well above the BoE’s 5.1% forecast, a key concern for some MPC members. Recent data also shows a strong economic bounce back from last year’s recession, potentially leading to renewed inflationary pressures.

All In Sync… sort of

Central banks in Switzerland, Sweden, the eurozone, and Canada have all made the first step in their rate-cut cycle, and they have done so without waiting for the Fed.

They are not oblivious to the pressure high rates in the US put on local currencies—increasing the cost of servicing dollar-denominated debts for these countries and prompting a flow of capital to the US—but they have started the descent.

The recent change in the US interest rate outlook has provided relief to central banks in other countries; they now have one less concern to deal with. Several developed markets, such as Canada and Switzerland, have made several interest rate cuts, which, in turn, increases optimism for rate cuts in the US.

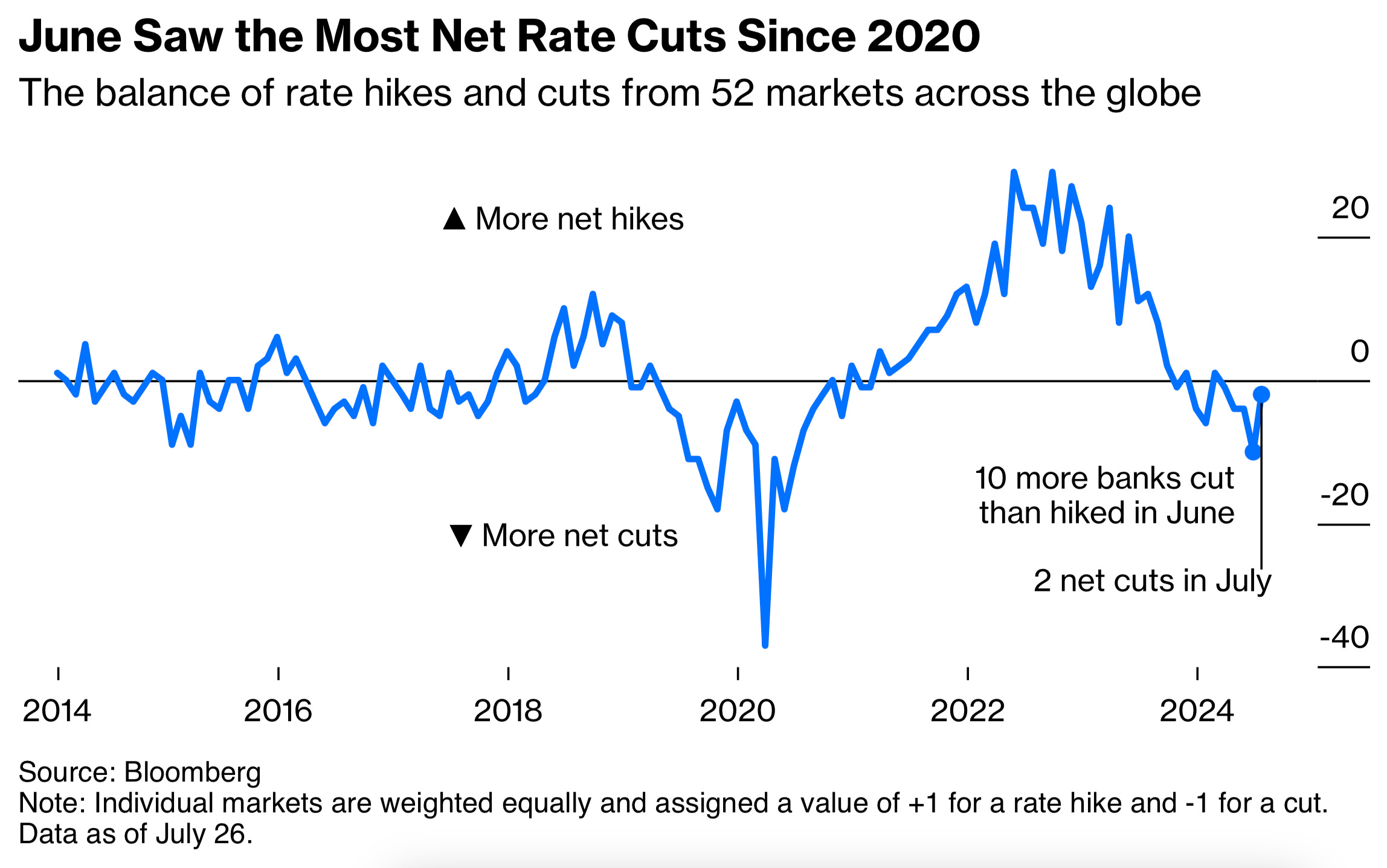

Look below at the Bloomberg diffusion index, which equally weights the impact of interest rate cuts or hikes by each of the 57 central banks. The visual clearly illustrates how the world is moving into a synchronised rate-cut cycle.

Navigating economic data has become pivotal over the last few years. Understanding how everything relates to and impacts the markets requires some effort.

For those who want a comprehensive explainer, it’s a good week for you. Citrini is out with the latest instalment of his series, ‘Global Macro Trading for Idiots’ (or GMTFI for short).

It’s thorough. It’s simple. It’s free. It’s worth reading:

Small Cap Summer

Albeit delayed by six months, the theme of rate cuts is finally coming to fruition in 2024. A cool inflation print earlier this month was the final element that saw rate markets cut a 26.5% chance of a rate hold from the possibilities.

Equity markets reacted, too:

The Russell has significantly outperformed since this data release, while the big-brother indices (S&P 500 and Nasdaq 100) have not only underperformed but have been negative.

However, note that the equal-weight S&P is up 3.5%. The drawdown in these indices has been tech-led. The move is dubbed “The Pain Trade”—money rotated out of the AI-driven tech industry and into other sectors that have been under pressure during higher monetary policies, ones that have also been heavily shorted by hedge funds.

That puts us in a new dynamic, one that we think will continue for the rest of 2024.

While “small-cap summer” may be upon us, there is still a lot of garbage in the Russell 2000. That is why the included stocks are in the Russell 2000 and not the Russell 1000 or the S&P 500.

It doesn’t take much digging to work out which sectors will benefit from rate cuts, and that’s what we’re here to discuss today.

Regionals

In the second quarter, US banks increased their provisions for credit losses due to concerns about defaults stemming from weakening commercial real estate (CRE) loans and rising interest rates.