Soft Landings Are Rare

Powell's descent down the monetary policy mountain will decide his legacy.

“It’s a consequential decision,” Federal Reserve chair Jerome Powell told reporters when asked about the pace of easing in June, adding: “You want to get it right.”

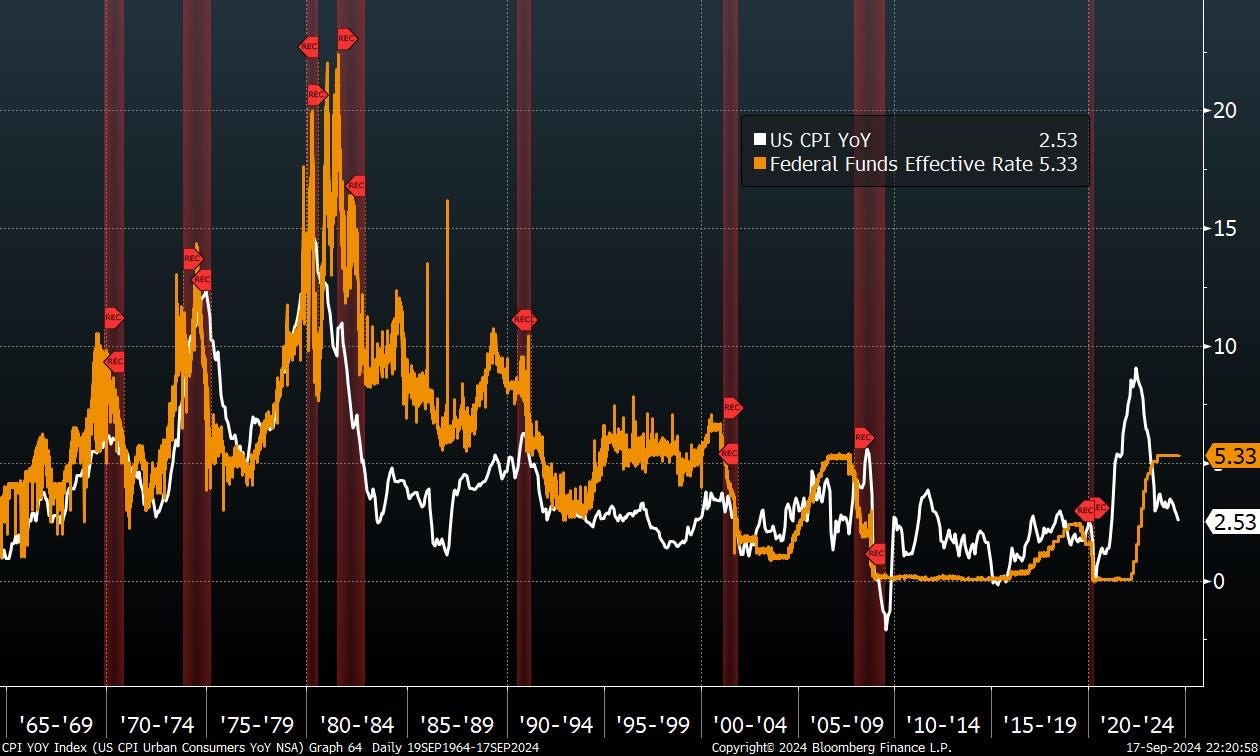

With concerns about rising inflation shifting to concerns about employment, the Federal Reserve is positioned to initiate the first in a series of anticipated interest rate cuts this week. Since the last Fed hike on July 26th, 2023, rates have been at an elevated level of 5.25 to 5.50%.

This is the beginning of a long-term easing cycle. The first step down this path is a consequential one. September 18th is also the quarterly meeting for the committee, so we are privy to the latest dot plot1. This aspect of the greatest FOMC of our lives (as the meme goes) may be more impactful and insightful than the size of the first cut itself.

Jerome Powell’s legacy as Fed chair will be remembered by the degree to which he navigates the global financial system through the largest contraction since the Great Depression and the worst inflation crisis in decades. Unfortunately for Jay, all the good work behind him will be forgotten if the eventual outcome is a hard-landing recession.

Today, we wanted to outline what we believe is needed for the Federal Reserve committee to orchestrate a soft landing. We then explain some factors and risks at play for the hard landing side of the debate. Finally, we present some trade ideas and how we are positioned for this initial cut.

Soft landing

With the objective of curbing an economy’s propensity for overheating inflation, central banks endeavour to judiciously elevate interest rates without sacrificing jobs or unnecessarily inflicting economic pain on people and corporations carrying debt.

A painless ending to a moderate economic slowdown would be referred to as a “soft landing.”

The term became prominent during the tenure of former Federal Reserve chair Alan Greenspan, who was widely recognised for orchestrating one in 1994-1995. Federal Reserve Chair Jerome Powell has also indicated that the Fed successfully achieved soft landings in 1965 and 1984, and was poised for another in 2020 before the intervention of the pandemic.

In short, it’s getting the right balance of not being overly restrictive on policy but also keeping control and moderating inflation.

Hard landing

A hard landing refers to a marked economic slowdown or downturn following a period of rapid growth.

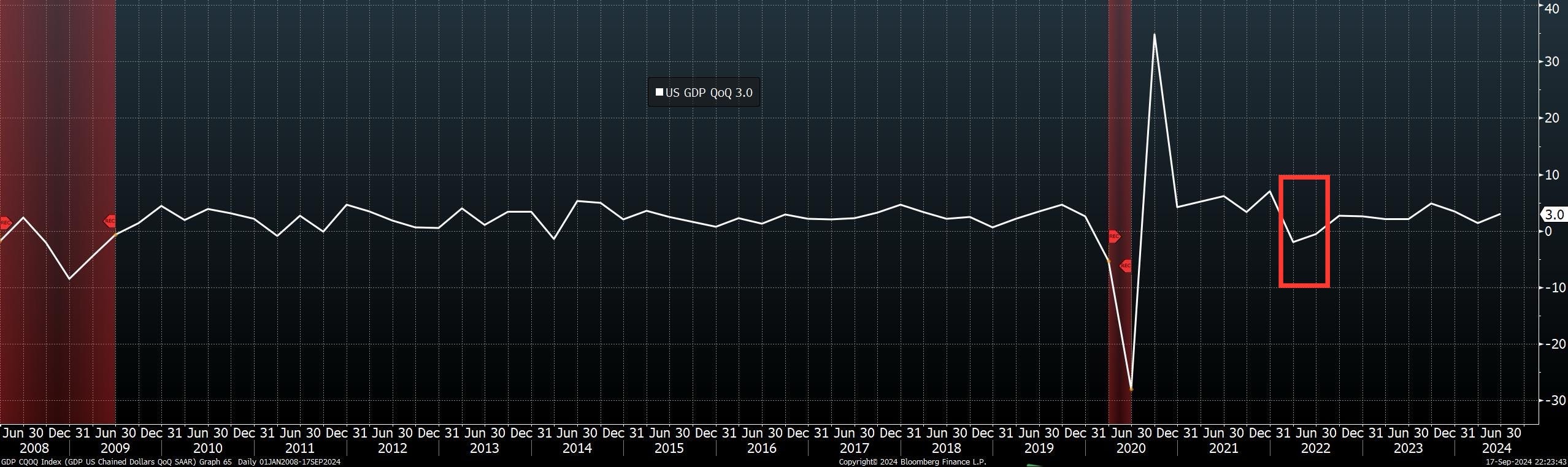

In contrast to the aforementioned events of a soft landing, a recession followed a >5% inflation peak in 1970, 1974, 1980, 1990, and 2008.

Looking at the data, we can see that soft landings are rare… but not impossible.

Inflation exceeded 5% in 2022. By the definition of a recession (two consecutive quarters of negative GDP growth), the economy was in a recession after the first and second quarters of 2022. The third quarter reversed the trend with growth in the gross domestic product, so we can refer to this as a mini-recession.

Typically, the duration of a policy-induced economic boom or the size of an easy money-fuelled market bubble directly impacts the difficulty of gradually retracting expansionary policy support to orchestrate a soft landing.

This dynamic can lead to a hard landing scenario, wherein the scaling back or cessation of expansionary macroeconomic policy may trigger a stock market collapse, financial crisis, or erosion of investor confidence. Owing to the acknowledgement, response, and execution delays in macroeconomic policy, these occurrences have the potential to swiftly evolve into a widespread recession, outpacing policymakers’ capacity to mount an effective defence.

The Fed’s navigation

Where is the Fed currently? Looking at the dual mandate (to promote maximum employment and stable prices), US inflation YoY is at 2.5%, and the unemployment rate is 4.22%. Ease too fast, and the central bank risks elevated inflation becoming entrenched. Too slowly, and it risks inflicting undue economic damage.