The Coldest Winter

Bitcoin’s volatility premium is freezing over.

Bitcoin was never bought for one reason. It was bought as digital gold, as an escape hatch from institutions, as a hedge against debasement, as a protest vote, and, for a younger cohort increasingly locked out of traditional wealth creation, as a beautifully volatile expression of financial nihilism. Each cycle offered a new explanation for why the price had to keep rising.

That’s what makes the latest sell-off more interesting than the usual crypto drawdown. Tuesday’s uncorrelated move took Bitcoin’s weekly decline to 11% and erased roughly $160 billion in market value. This does not mean Bitcoin is dead. Assets do not die just because their holders have a bad week. But Bitcoin’s newfound characteristics suggest that the trade has entered a different phase.

In our view, the old pitch relied on volatility, purity, and unfinished upside. All three now look weaker. Speculative capital has found a more exciting outlet in AI, semiconductors, and memory stocks. The largest symbolic buyers are no longer quite as mechanically one-way as the market assumed. And the great institutional and regulatory catalysts that once sat in the future have largely arrived.

Bitcoin has not lost its relevance, but it is increasingly losing its edge. The asset that began as a rebellion against the financial system is now liquid, institutionalised, ETF-wrapped, policy-recognised, and increasingly well-behaved.

Bitcoin has become what it swore to destroy.

The Monopoly on Volatility

Part of Bitcoin’s recent underperformance can be explained by a shift in where speculative capital now believes the best trading assets are located to generate large short-term returns.

For much of the last cycle, Bitcoin was the high-beta expression of liquidity and retail risk appetite for those chasing what was coined “financial nihilism.” This is the belief that traditional methods of building wealth are broken or inaccessible, driving the younger generation to an “all or nothing” mentality via dumping money into highly volatile assets.

Throughout periods of 2024 and 2025, it offered these nihilistic speculators regular large price moves with perceived permanent narrative optionality (institutional adoption, CLARITY Act, etc.). More than that, Bitcoin contained a market structure loose enough for momentum to feed on itself.

That proposition has become less compelling as the asset has matured. ETF ownership, institutional hedging, deeper liquidity, and a broader derivatives market have made Bitcoin more investable, but also less feral. In other words, the same institutional adoption that helped legitimise the asset has also dampened some of the volatility premium that made it attractive to retail and pro traders in the first place.

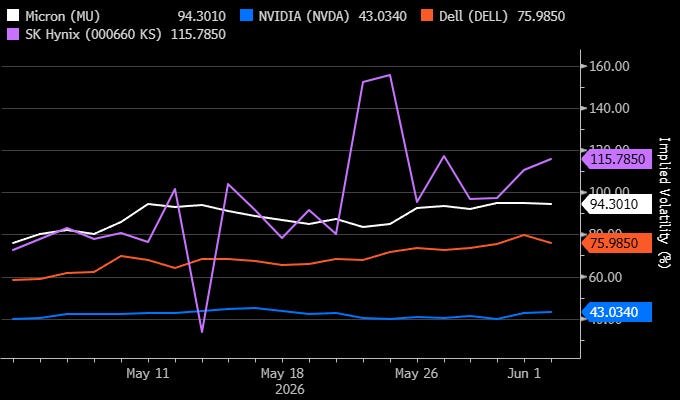

For example, the one-month ATM implied vol for Bitcoin is currently 36.9. Contrast this to some large-cap equity names that have been the flavour of the month (and arguably the past year).

The implied vol is direction agnostic, but that’s not the point we’re trying to prove here. Traders don’t really care whether the asset is moving higher or lower, they just want the potential for future price movements to be high. The greater the potential volatility, the greater the chance of loading up on quick riches.

Speculative capital that seeks these riches is not loyal. It follows realised movement and implied volatility. If Bitcoin is no longer offering the sharpest upside tails, traders will look elsewhere for volatility with a better story attached.

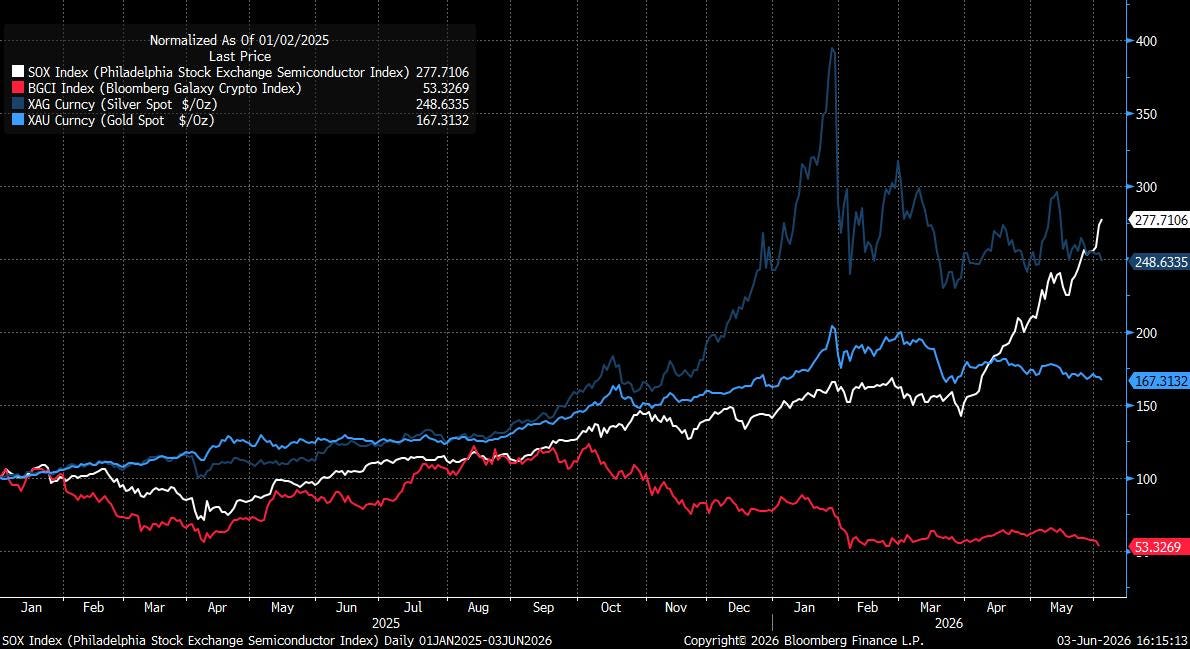

As we’ve just visually depicted, that story right now is in AI infrastructure, semiconductors, and memory.

They contain the same formula as Bitcoin did a couple of years ago. We’re talking about violent moves, strong narrative momentum, and a credible structural growth backdrop. If you removed the legend from the chart below and asked someone two years ago which normalised return was linked to the Galaxy Crypto Index and which was linked to the semiconductor index, gold, and silver, we’d wager the majority would get it wrong.

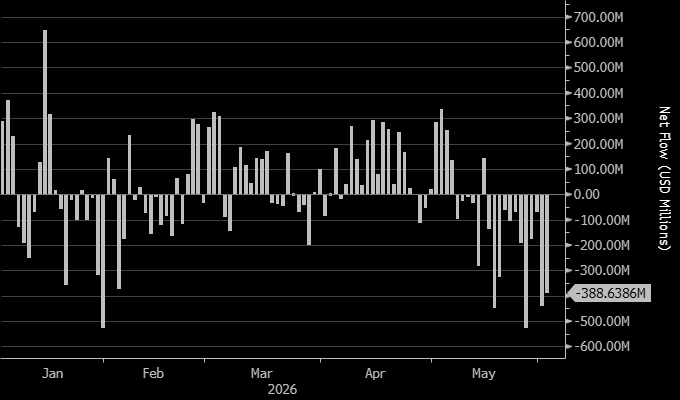

To a certain extent, this thesis extends into the future. May was a tough month for outflows from IBIT, and logically this cycling out of Bitcoin hasn’t just found a home in the money markets. Money is actively flowing out of crypto and into higher-volatility assets, which, in turn, makes those assets more volatile and attracts more capital. That’s the problem for Bitcoin going forward. It has not entirely lost its narrative; it has simply lost its monopoly on volatility.

Bitcoin ETF flows turn persistently negative over May…

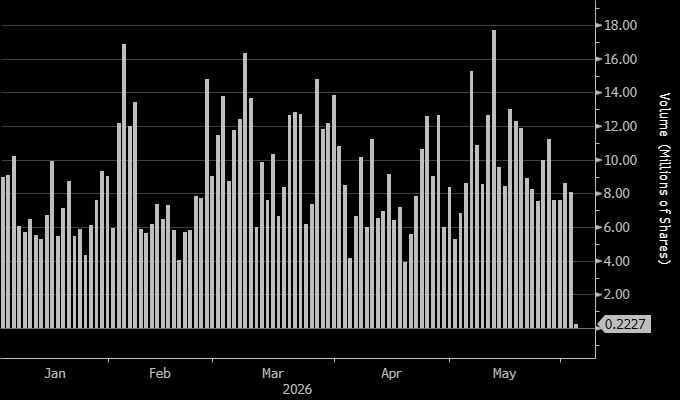

…while VanEck Semi ETF trading volume enjoyed a bumper month.

While the AI boom is grounded in genuine fundamentals, it has also become the latest vessel for financial nihilism, offering a new arena for speculative hope at a time when crypto’s promise of escape no longer feels quite as compelling.

Sayl-ing Away

Bitcoin’s short-term weakness has also been amplified by a more subtle confidence shock, as news broke that Saylor’s Strategy sold Bitcoin. In absolute terms, the sale was irrelevant. A disposal of 32 BTC against a treasury still measured in the hundreds of thousands does not change the supply-demand balance of the asset.

According to Citi, the sale was anticipated as Strategy had signalled plans to dispose of certain tax-disadvantaged bitcoin holdings during its Q1 earnings call as part of a portfolio optimisation effort.

But markets do not trade only on size. They trade on symbols, and Strategy has been one of the most important symbols in the Bitcoin ecosystem. Michael Saylor built the company’s public identity around the idea that Bitcoin was not a trading asset, but a permanent treasury reserve. Strategy was not supposed to sell Bitcoin. Strategy was supposed to buy Bitcoin, hold Bitcoin, issue paper against Bitcoin, and then buy more Bitcoin (even if this doesn’t actually make sense in the real world).

So when we boil it down, the issue is not that 32 coins hit the market. The issue is that one of the flag-bearing corporate holders has introduced a new uncertainty into what had previously been a very simple story. For years, the appeal of Strategy and the wider Bitcoin treasury cohort was that they behaved almost mechanically. They bought, they held, and they reinforced the idea that institutional adoption would create a one-way absorption vehicle for supply. The moment that model becomes conditional, even at the margin, the market has to reprice the narrative.

If the most evangelical holder can sell a small amount to fund obligations, then investors have to at least consider whether other Bitcoin treasury vehicles might also become sellers if financing costs rise, equity premia compress, or balance sheet pressure builds.

In the age of misinformation on social media and the plethora of so-called crypto gurus, it’s also hard for some retail traders to see the wood from the trees. For anyone who instead listens to their favourite crypto doomsayer, the story can easily be spun into Strategy starting to sell holdings due to being underwater, etc. Again, it’s the narrative, not the size.

Bitcoin has not been damaged by the size of the sale. It has been damaged by what the sale says about the purity of the holder base.

“We’re So Early”

We touched on it earlier, but another factor at play is that crypto bros are no longer early to the party.

For much of the last decade, Bitcoin was the cleanest expression of being early to the next financial architecture. Institutions hadn’t arrived. Regulators had not fully turned. ETFs had not been approved. Traditional finance had not built the pipes. Buying Bitcoin felt under-owned and under-discovered.

That is harder to argue today, and therefore pushes it more towards a maturing asset where reasons for explosive growth are harder to justify. Institutional adoption has already happened. Spot Bitcoin ETFs are live, asset managers have products, custody has improved, corporates have put Bitcoin on balance sheets, and the language of digital assets has been absorbed into mainstream finance.

Let’s also not forget that the regulatory environment (particularly in the US) is also about as favourable as it has ever been. Bitcoin has already received the policy and institutional recognition that bulls once argued would unlock the next leg of demand.

The crypto crowd might argue that the “we’re so early” tagline can’t apply to AI either, but we’d disagree. Semiconductors have been a popular feature of the AI trade since the unofficial beginning of the trade (the launch of ChatGPT in November 2022). The picks-and-shovels approach. And yet, March 2026 may have presented itself as the ideal time to go long semiconductors in this cycle.

For Bitcoin, the problem is not that the story has disappeared. The problem is that the story has matured. The easy narrative tailwinds have been harvested. The asset is still investable, but it no longer carries the same informational edge.

The Bottom Line

To reiterate, we’re not perma-bears on crypto. We could argue why a diversified portfolio might still deserve small allocations to the major coins. However, the narrative of Bitcoin heading “to the moon,” with some forecasting earlier this year of a $250k target by the end of 2026, just lives in fairy land.

It no longer has the volatility appeal, it’s no longer the early trade, and short-term actions from Saylor expose the sensitivity of the market.

Crypto isn’t dead, but the investment pitch has changed over the past six months more than we believe some people appreciate.

AP

Say it louder for the people in the back! Great read sir.

What I find most useful in this framing is the observation that institutionalisation and volatility premium are inversely related. That is not a Bitcoin-specific dynamic. It is a structural pattern that shows up across asset classes. Private equity delivered outsize returns when it was under-owned and under-regulated. Emerging markets carried a genuine risk premium before dedicated EM funds made them accessible.

High yield offered real compensation before it became a standard allocation. The mechanism in each case is the same: the process of legitimising an asset class compresses the premium that made it worth owning in the first place. Bitcoin has followed the same arc faster than most. The more interesting allocator question is where the next genuinely under-owned, high-volatility narrative with structural backing currently sits. The piece implicitly answers that: semiconductors and AI infrastructure in March 2026.

In my view, the more honest version of that observation is that those assets are now doing what Bitcoin did in 2021, attracting speculative capital on a legitimate fundamental story, which means they are also beginning the same institutionalisation process that eventually compressed Bitcoin's premium.