The photo of Venezuelan President Nicolás Maduro handcuffed in a Nike tech fleece after being abducted by the US on January 3rd should have alerted us that Q1 was going to be anything but ordinary.

Yet from a macro perspective, Q1 opened with a familiar tone. Disinflation narratives fraying at the edges, commodities reasserting themselves as the marginal driver of macro, and equity markets still leaning into a narrow set of secular winners.

That equilibrium of constrained volatility did not last for long.

With the benefit of hindsight, writing in April, what followed in Q1 was a period defined by an abrupt regime shift. More specifically, the conflict in Iran (which began on February 28th) provided a sharp transition from a pre-conflict environment to a global headache. It forced markets to confront the reality that geopolitics is no longer a background variable but a primary driver of cross-asset pricing.

For macro traders, the period was one in which a year’s worth of P/L could be made or lost in a single day. When considering moves in oil and Euribor futures, we can reframe the timeline to hours.

The distinction between thematic investing and tactical positioning blurred as macro shocks forced even the highest-conviction ideas to pass through a liquidity filter. This ultimately punished anyone that though those forces would play out in a straight line.

What follows is our attempt to map that transition, assess where we were right, where we were not, and how the experience reshapes our positioning into Q2.

Q1

The portfolio entered the year leaning heavily into the themes that defined the tail end of 2025: commodities, defence, and the evolving AI stack. In the opening weeks of January, it felt as though we were playing a game of Texas Hold’em where we had been dealt the “bullets.”

However, the quarter can be categorised into two definitive dynamics: pre-war and post-war.

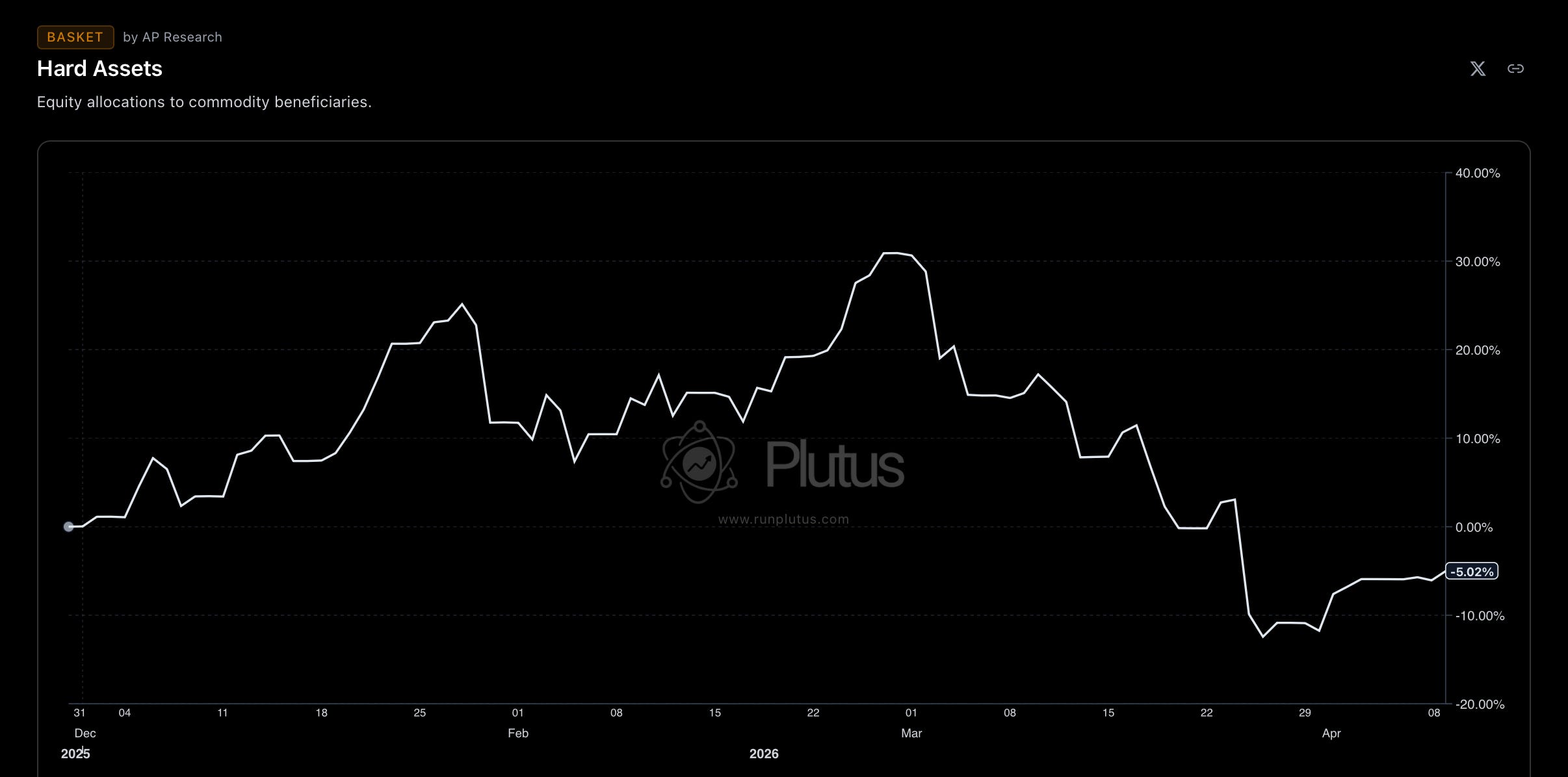

Commodities led the charge, as our thematic basket gained 30% into the end of February as the “debasement” narrative took hold. The momentum was checked by the silver crash in late January, but ultimately the names held up strong considering. The real momentum unwind in metals came after the start of the Middle-East tensions and forced a recalibration of these holdings and our “hot hand” portfolio.

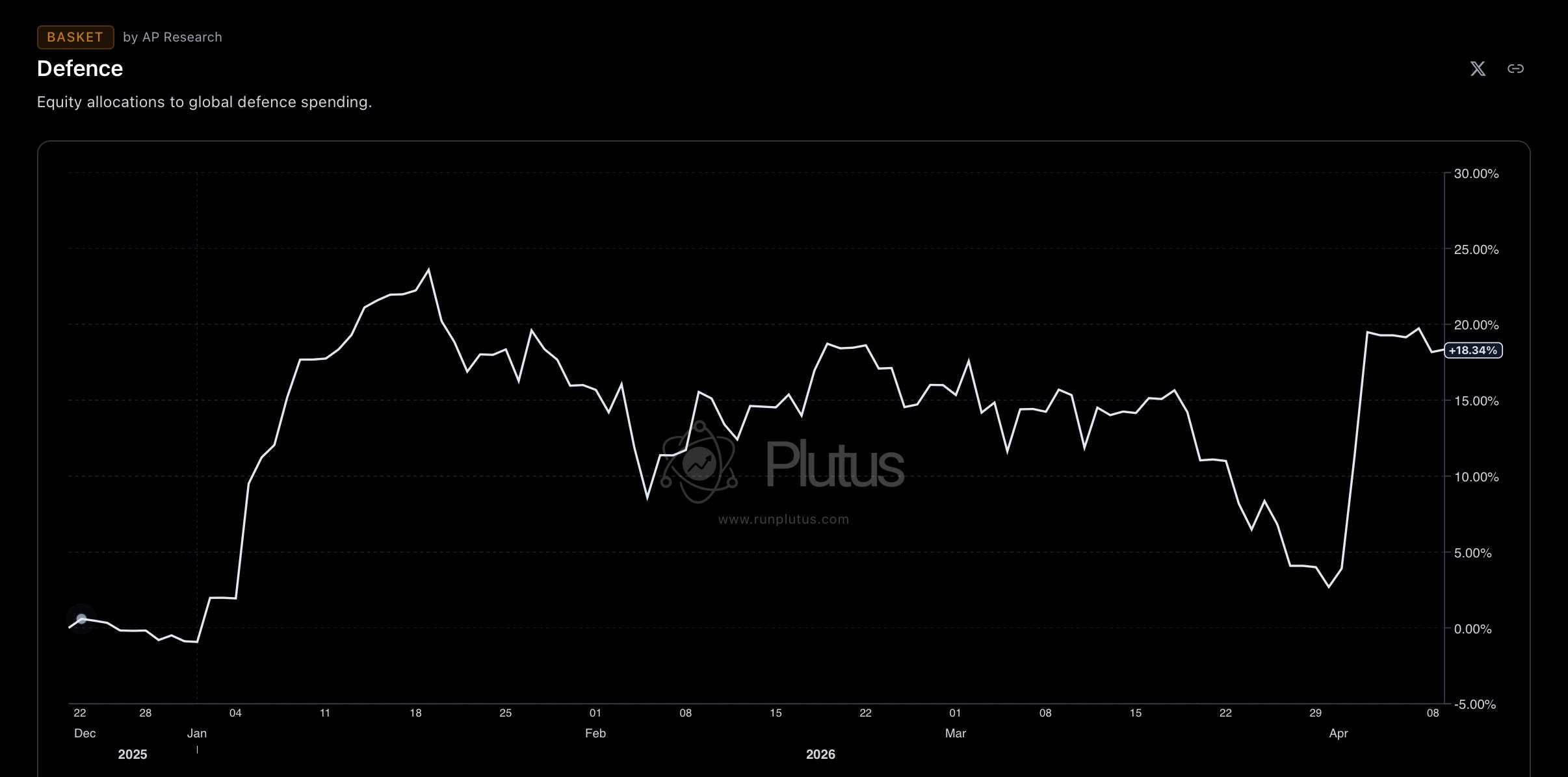

Our defence exposure acted as a necessary hedge to this volatility, providing a steady return while the macro dust settled. Global geopolitical friction is now a permanent feature of the investment landscape.

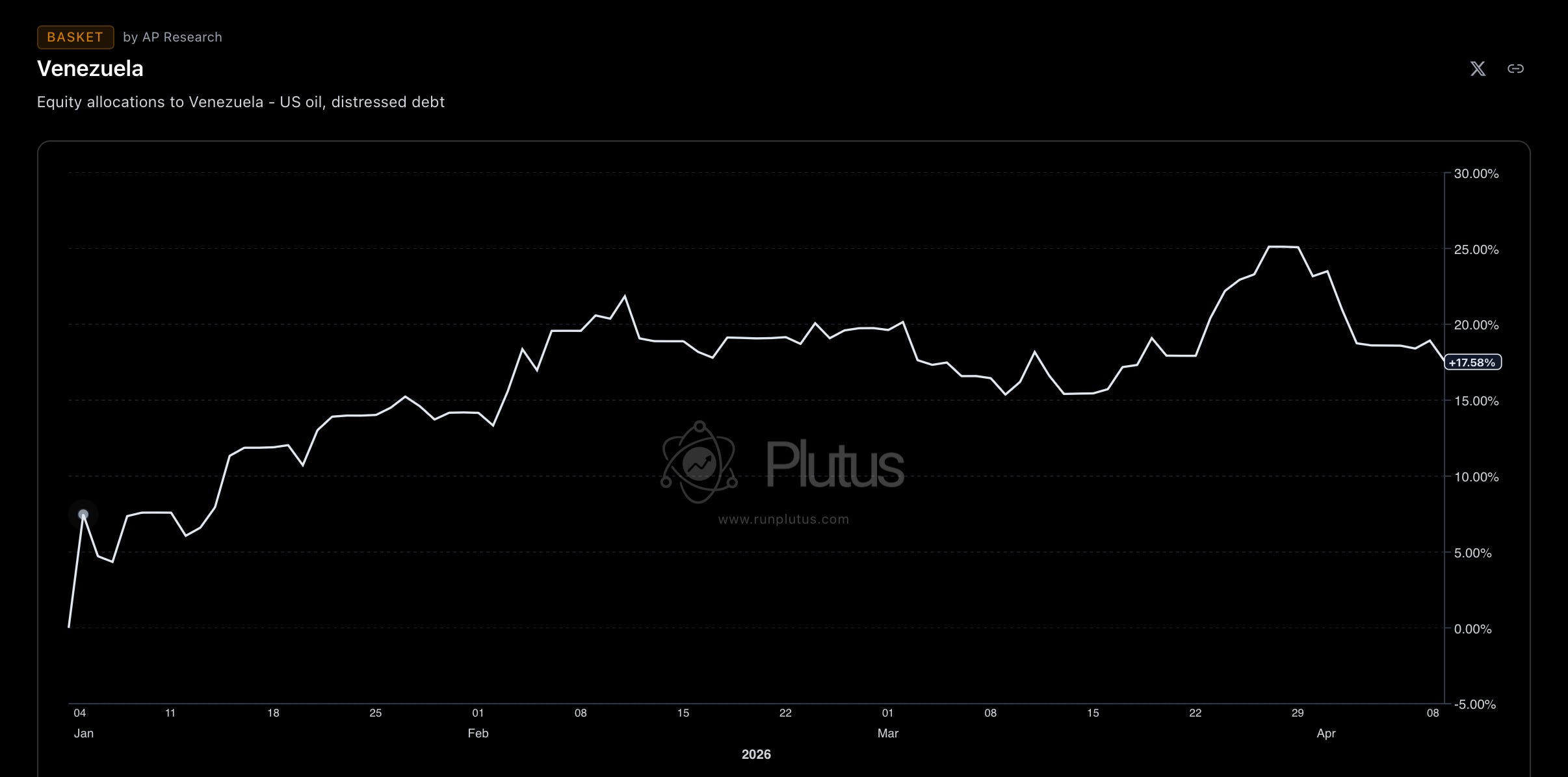

The sudden removal of Maduro in Venezuela provided the catalyst for our idiosyncratic Venezuela basket, which capitalised on the prospect of regional stabilisation and debt restructuring to return 23.5% over the quarter since inception.

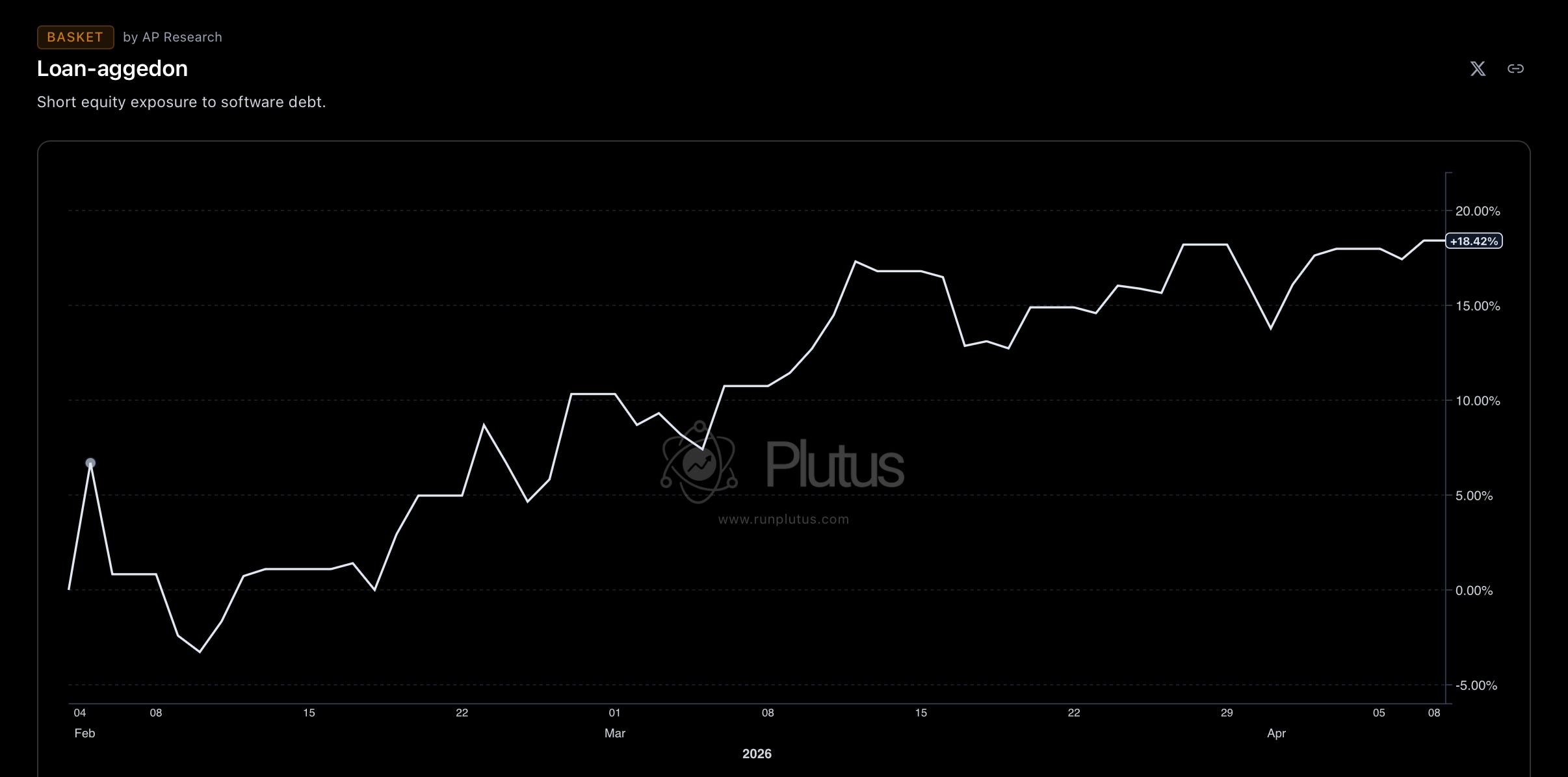

We also saw significant alpha from our alternative asset manager basket, which rose 18% since its inception in early February. This thematic was an expansion of a short trade that we started in Blue Owl (OWL US) in Q4 of last year. As the Software-as-a-Selloff trade consumed markets in the form of the latest AI development, we increased this single trade into a basket of short trades in BDCs, looking to gain from rising stress in private credit. Markets were already punishing private credit before the war, and a risk-off environment to end the quarter only aided these positions.

The market has a way of punishing hubris. The outbreak of hostilities in Iran shifted the board entirely. The dynamic played into your hand if you were a commodity-focused shop (notably Andurand, finishing Q1 up 31.1%), but the broader impact for strategies was a tougher one, and we did not go unscathed.

The most fascinating (and painful) development was the behaviour of gold. Despite its status as a geopolitical hedge, gold fell 24% following the breakout of the war. As we detailed in our market memo, we witnessed a decoupling: sovereigns who had spent years building gold reserves were forced to use the metal as a “funding vault” to acquire dollars for oil. The fundamental fear bid was overwhelmed by a need for liquidity.

Read more: “A Chink in Gold’s Armour”

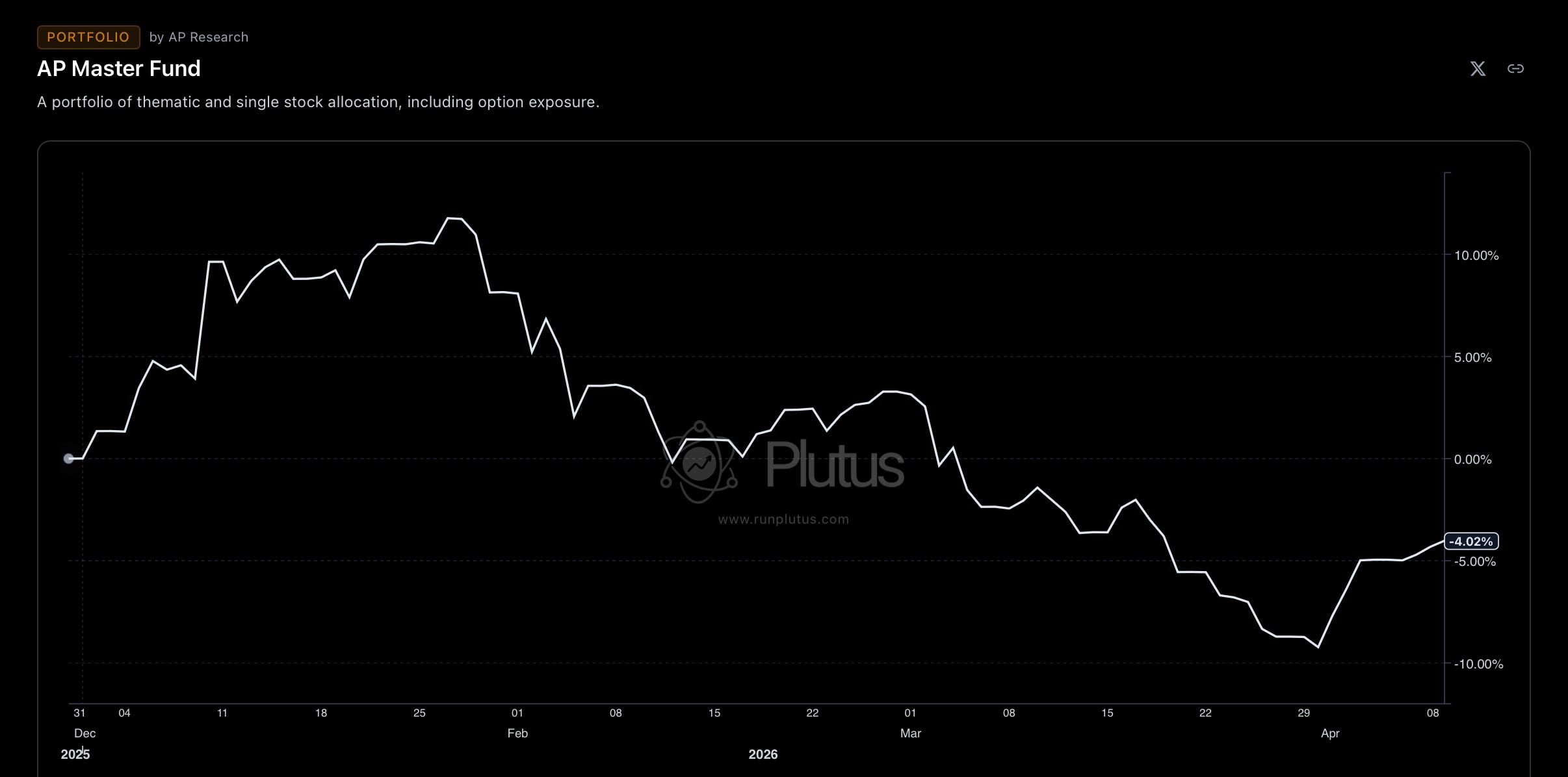

To protect the core, we spent mid-March raising cash and reducing exposure across the portfolio. This defensive posture cushioned the end-of-quarter sell-off in the equity portion of the portfolio (tracked on RunPlutus).

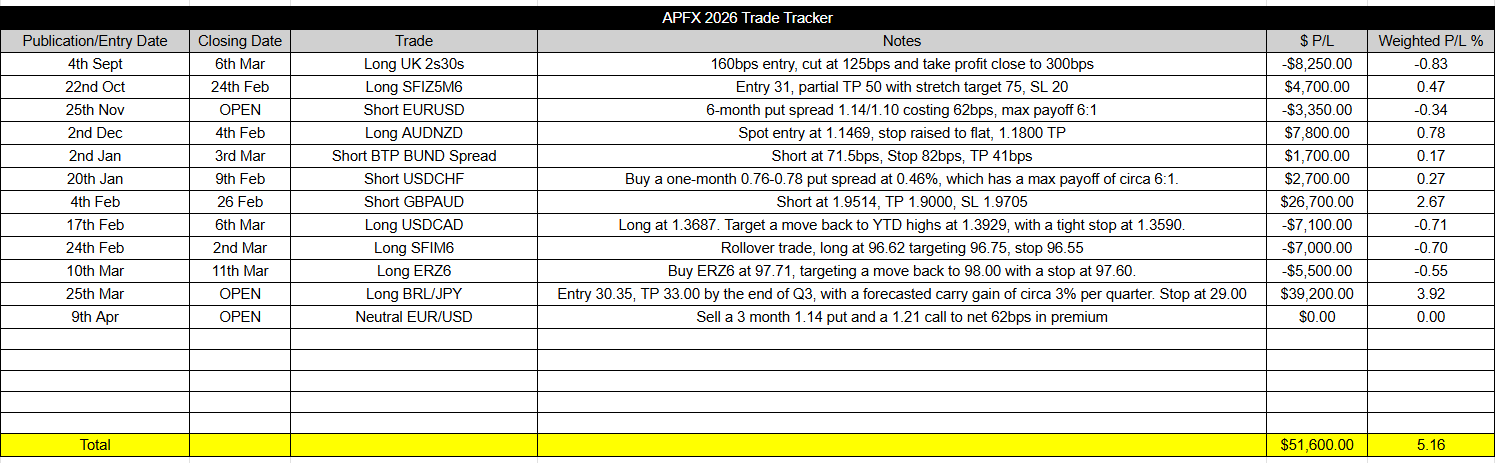

FX & Rates Portfolio

Our dedicated commentary channel for FX and Rates is APFX Research, where users can find regular trade notes and a portfolio trade tracker.

YTD trades and performance can be found below: