Top Trade Ideas - January 13th

Inflation data takes centre stage globally.

The first full week of the year didn’t disappoint. NFP data came in hotter than expected, and the unemployment rate fell from 4.24% to 4.08%. Good news is bad news again for stocks. A strong labour market means less concern for the Fed to ease financial conditions. Markets are pricing just one cut this year.

All U.S. indices ended the week lower. The VIX crossed 20 to end the week.

The dollar continued its rally higher as yields soared. The U.S. 30yr hit 5% for the first time since November 2023. Likely, hedge funds feel under-positioned, as was seen by the acceleration in EURUSD selling. USD broke to new cycle highs vs G10. That brings more negative impacts for EMFX.

Oil continued its quiet rally higher, now up for the past three weeks.

The Week Ahead

U.S. inflation data will be top of the agenda in the week after recent very strong jobs data and could cause investors to scale back expectations for interest-rate cuts even further.

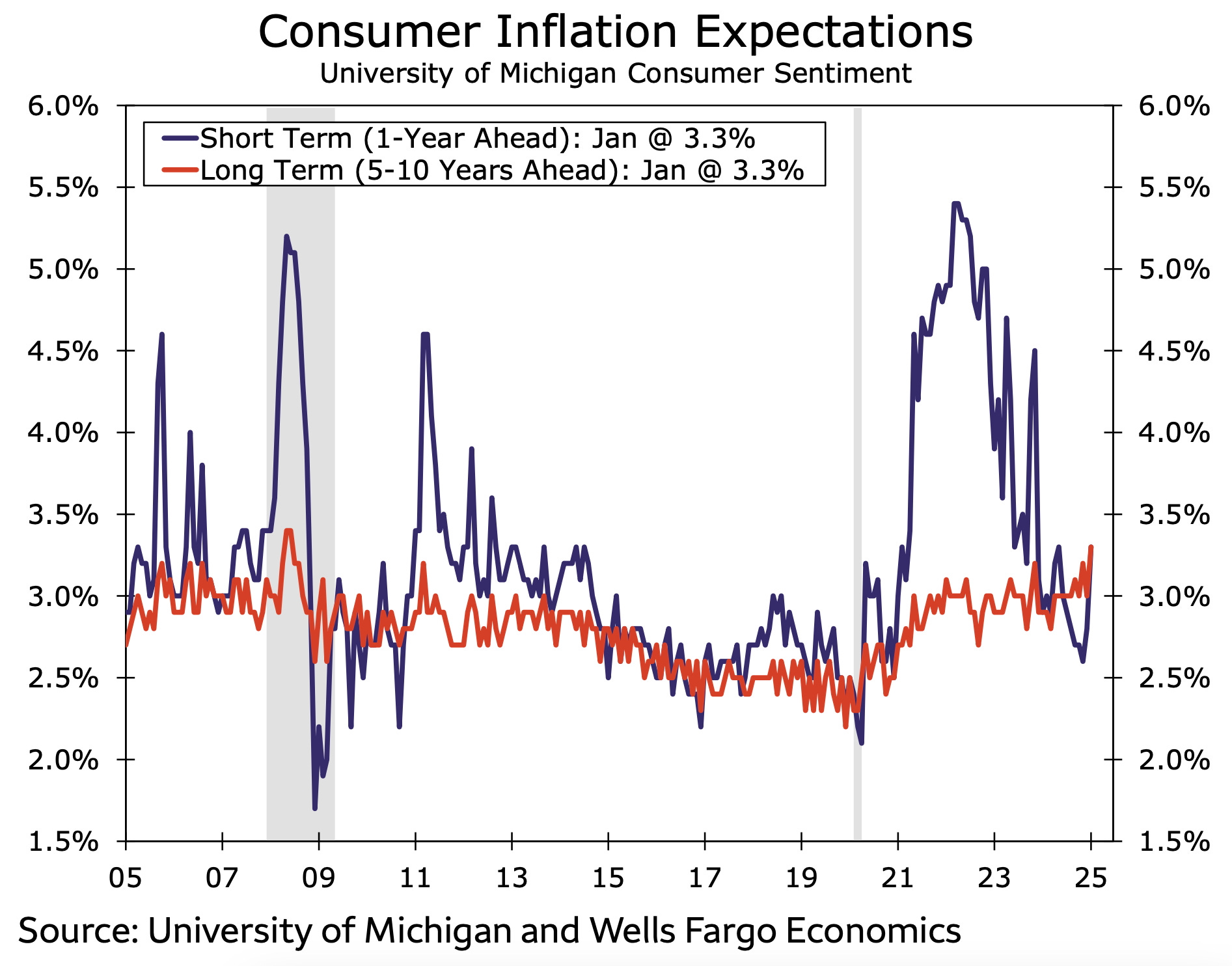

Financial markets will have to wait for hard data on inflation with the release of the CPI report on Wednesday. However, last week’s survey of consumer sentiment from the University of Michigan points to a significant rise in inflation expectations.

Focus will remain on bond markets given a recent rise in yields, particularly in U.K. government bonds. U.K. inflation data will, therefore, garner particular attention.

In Asia, data from China will show whether the world’s second-largest economy hit its growth target last year.

If you are not yet a premium subscriber, you can manage your account here.

FX

The DXY continued to push higher, fuelled on Friday by the strong payrolls print and fall in the unemployment rate.

Last week, we put out a bearish EUR/USD option structure, which is ITM, alongside the other put spread from the trade ideas in December. We don’t want more downside exposure but acknowledge that not all readers will have put on either of these positions.

U.S. inflation, U.S. retail sales, etc., out this week present another run for EUR/USD to test parity, so we’ll hold out on our options but present another idea for those still on the fence / without existing exposure to this move.

TRADE IDEA - SHORT EUR/USD (AGAIN)

Buy a 2-week EUR/USD 1.02 strike put with a 1.05 KO costing 0.5% for a circa 3:1 RR on a sharp parity move

GBP struggled last week, with woes in the Gilt market pushing the 30yr to the highest level since 1998. The fact that GBP weakened as well is a clear sign that this added yield differential versus other G10 currencies isn’t being taken as a good sign.

However, we don’t feel this is a Truss 2.0 situation (we wrote about that in detail last Friday here) and are actually more inclined to leave an order to buy this as a dip. We like to match it up against JPY, given our continued bearish view of the Yen heading into another CB meeting where Ueda and Co. could disappoint the market.