Trading the Tariff Man

Tariff winners, commodities, the great rotation trade and the curve flattener.

Trump dampened everyone’s weekend when he announced tariffs on Canada, China, and Mexico. As expected, the market opened lower on Monday. However, true to form, investors quickly seized the opportunity to buy the dip, making it back-to-back Mondays of opportunistic cash deployment. This response indicates that markets still view these threats as a form of negotiation leverage. After delays to these levies following conversations with Mexican President Claudia Sheinbaum and Canadian Prime Minister Justin Trudeau, we’re now back in a wait-and-see environment.

The President has shown he’s willing to destroy long-standing alliances for minor, mostly symbolic concessions. It seems like an overstatement to call that a win. At least we can all say, “I survived the Great Trade War of February 3rd, 2025.”

This tariff tussle has brought several thoughts to mind, and we also had the first Treasury quarterly refunding announcement (QRA) under new Secretary Scott Bessent. The QRA was mostly a snoozefest, but there are still a few takeaways. As we draw close to the end of the week, we wanted to sit down and write out our thoughts on it all, from the tariff winners, commodities, the ongoing global and sector rotation trade, and the curve flattener. A slightly different approach to usual, but beneficial nonetheless.

Lots of Losers, Few Winners

The dollar is the go-to haven for tariff talk. However, with Trump’s rhetoric softening and the allowance for negotiations from Canada and Mexico, it still feels like “The Art of the Deal” is in full force. Markets probably echo that view, as the dollar index is lower for the week and not far from year-to-date lows, and our bias is still leaning towards the dollar being lower in the mid-term. Tit-for-tat tariffs are a zero-sum game and ultimately do not benefit either side. Constructive trade deals, on the other hand, can be advantageous for both parties. Either way, heightened uncertainty will likely boost demand for other traditional safe havens such as the Swiss franc, Japanese yen, and gold.

Commodities

Gold has risen by over 6% since the beginning of the year. Since Donald Trump’s first-term tariffs rattled global trade, and with the pandemic’s aftermath still reverberating, the average of Bloomberg Commodity Index rose about 30%, from an average of 80 during his first term (2017–21) to around 104 today. Now, with new tariffs being threatened, a similar cycle of turbulence may be unfolding again.

Tariffs aimed at raw materials, such as China’s export restrictions on tungsten and the U.S. tariffs on liquefied natural gas, can significantly increase price volatility. Businesses rush to protect themselves against rapidly changing input costs. Sectors ranging from electronics to defense feel that pressure.

In 2018, Trump’s steel and aluminum tariffs caused a spike in volatility. Manufacturers faced soaring funding costs, leading many to put major projects on hold. As a result, stock valuations for mining and production companies saw significant fluctuations.

This instability acts like a hidden tax on corporate profits and dampens productive investment. Generally, firms tend to postpone large expenditures when faced with uncertainty, which reduces supply and drives prices up. On a broader scale, central banks, already grappling with persistent inflation, might have to adopt a less dovish stance than they would prefer at this point in the easing cycle, setting the stage for increased stagflation risks as concerns about growth intensify.

Economic Impacts

The broader economic impact extends beyond the nations directly involved. Analysts estimate the risks associated with tariffs could reduce U.S. GDP by approximately 1.2% while pushing core PCE up by around 0.7%. This situation threatens the momentum of U.S. equities, which have thus far been supported by strong domestic growth.

The ongoing conflict adds complexity to the outlook for monetary policy and the bond market, as inflation emerges as a more pressing concern. With the U.S. economy expected to slow down due to these factors and China already facing challenges in its recovery, emerging markets will likely remain under pressure. As risks of retaliation mount and uncertainty lingers, we can anticipate heightened volatility across FX, equity, and fixed income markets.

Deer Point Macro posted a great article on the economic side of tariffs. His deep-dive says it better than we can. You can read it here.

The Great Rotation Trade

Is it upon us? 2024’s laggards are gaining significant momentum at the expense of last year’s winners. Growing caution around the AI trade is one of the driving factors of the focus on Europe and financials so far this year.

The top three markets of 2024—Taiwan, the U.S., and Japan—now rank fifth, eighth, and third-worst among the 23 major markets this year. Conversely, France and Switzerland, among the worst performers in 2024, have surged to third and fourth place. Meanwhile, Germany and Italy maintain their positive trajectory, yielding the best returns this year.

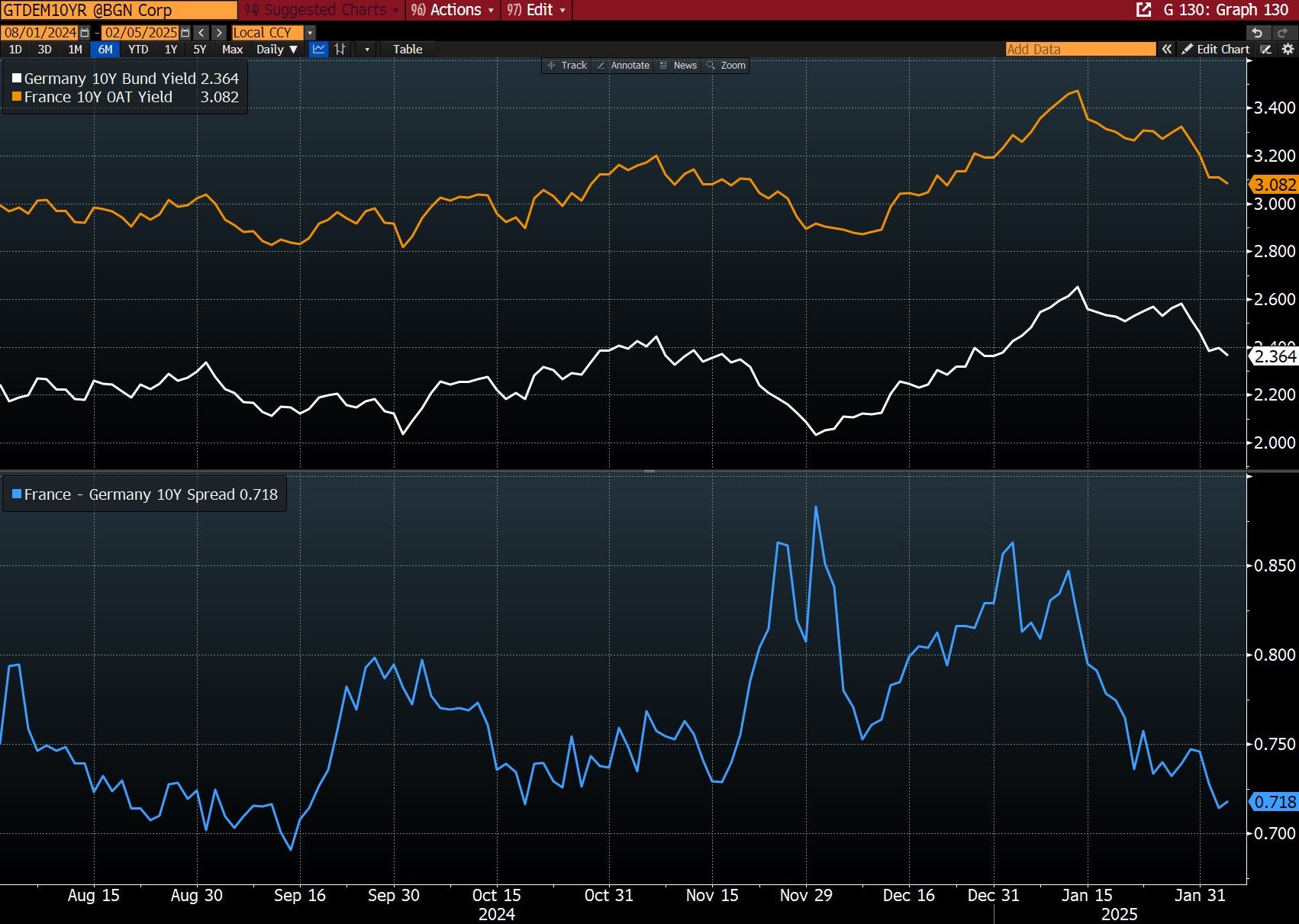

Bayrou survived a no-confidence vote this week, which was largely expected. The OAT-Bund 10yr spread closed at 72bps on Wednesday, down from 85bps in January. French stocks have climbed almost 7% this year. The political turmoil has cost France €12bn, or €175 per person, but it looks like the worst is behind them. That’s a story similar to that of the rest of Europe.

A lull in tariff headlines looks to be proving key for most of Europe, both in bond and equity markets. The boost to stocks is obvious, but the calm can also help bonds by reducing the immediate risk of more inflation. If markets are now in a tariff on-tariff off dynamic, rather than a classic risk on-risk off one, it might be that we see bonds and stocks move in the same direction a lot more in the days and weeks ahead.

Sector Shift

A shift in sector performance is also becoming apparent as we head into 2025. Technology, the leading sector globally in 2024, faces challenges at the start of the year. This U.S.-heavy sector may continue to grapple with the fallout from overly inflated valuation levels as the market reassesses the impact of emerging competitors and prepares for tougher earnings comparisons ahead.

Domestic Winners

It is not only countries that lose in a tariff war. Many companies get pulled into the sinkhole of higher prices and lower margins. All in all, many more companies lose than win in a trade war.

For example, Trump promised to impose tariffs on John Deere if they planned to move some production to Mexico. Major global players like Pepsico and Unilever, which have invested in sourcing from Mexico, could face substantial tariffs. International firms such as Danone, Coca-Cola, Chiquita Fresh North America, Dole, Mondelēz, and Ferrero might get caught in the crossfire of these tariffs, too. Constellation Brands, known for importing Corona, Modelo, and Pacifico from Mexico, could also see its products hit with increased tariffs. Small businesses might struggle to cope with these rising costs, as their profit margins are squeezed. We’d also be concerned about the implications of tariffs for the discounters like Five Below and Dollar Tree given how much they import from China and their fixed price points.

On the flipside, operations in countries with lower tariffs could spring up, as some companies look to strengthen their U.S. presence.

But where do you turn if an investor wants to keep U.S.-focused long exposure? Our bias leans towards domestic manufacturers. A big company that comes to mind is Tesla. We’ve previously outlined the bull case for the stock with Musk and Trump’s alliance growing.

YETI is another name that we highlight as one that can avoid tariff volatility. The company has some coolers and equipment manufacturing in Mexico (~5% Mexico sourcing estimates) and has no Canadian manufacturing exposure. 82% of sales are within the U.S. However, they have more exposure to China, but so far, levies are lower towards China than the Americas (10% vs 25%).

Small caps may be an angle here. While some companies generate revenue internationally, small-cap stocks tend to be more U.S.-centric than large-cap counterparts with substantial global operations. However, the risk at play with small caps is the debt. With the interest rate picture indicating a moderate easing in 2025 (2 cuts in 2025 compared to 4 cuts priced in the early part of Q4-24), the burdens to interest payments in debt—small companies use higher amounts of debt to fund operations—can weigh on the index.

Curve Flattener

The resurgence of tariff risk has led to a flattening of the 2s10s yield curve. Recently, short-term bond yields have risen due to renewed inflation concerns stemming from trade announcements. This situation contrasts the 2018-19 trade war, which resulted in lower yields as recession fears took hold.

Today, markets view tariffs as inflationary in the post-pandemic landscape, as evidenced by rising inflation expectations. There are indications that businesses might exploit these tariffs as a rationale for increasing prices, which could further fuel inflation. Additionally, the ongoing imposition of tariffs could heighten anxieties about economic growth, hinting at the possibility of further flattening of the yield curve.

Bessent and the Trump administration are in active pursuit of lower 10-year yields, but, ironically, it’s their own threat of tariffs that will stymie those efforts.

QRA

There was a sigh of relief on Wednesday as the U.S. Treasury decided to keep the size of its upcoming debt sales unchanged. This move eased concerns about an increase in the supply of longer-term bonds under the new Treasury Secretary, Scott Bessent. Coupled with data indicating a healthy labor market, there are strong reasons to believe the yield curve may continue to flatten. However, Friday’s labour data can throw a spanner in the works on this front. NFP is expected at 1169k v 256k previous. UER is expected to stay steady at 4.1%. We’ll see what happens there.

Bessent had previously criticised the issuance strategy of his predecessors, which raised the possibility of increasing long-term supply. However, the Treasury maintained steady debt sales at $125 billion for next week and confirmed that it plans to keep nominal coupon auction sizes stable “for at least the next several quarters.” This implies that increases to coupon auction sizes are unlikely until 2026.

We’ll wrap it up there as there are lots of thoughts across several areas of the market. Meme of the week goes to the below. We’ll see if Trump gets what he wants or has shot the American economy in the foot.

Thanks for reading. Leave a like if you enjoyed it and are still here. See you on Sunday.

Happy trading,

AP

Want a free tariff calculator https://careerchronicle.mysamcart.com/checkout/5-minute-tariff-cost-calculator