Can Tesla And Netflix Earnings Keep The Party Going?

As the NASDAQ keeps on surging, we preview two big earnings for next week to see if either will help or hinder the rally.

We feel the NASDAQ needs some strong earning beats in coming weeks to maintain the run higher.

Tesla have room to outperform given the price cuts already showing higher production numbers.

Netflix could struggle given the high benchmark, with EPS due to fall by 12% YoY.

The rally in the NASDAQ 100 has continued this week, fuelled by falling inflation (CPI at 3% is the lowest level in two years) and a resilient labour market.

Despite the index creeping into overbought territory when looking at the RSI indicator below, the technical break above 15,250 could spur even further gains next week.

Yet besides pure price levels, a key factor will be the impact of earnings releases from constituent heavyweights. Today we preview two of these, namely Tesla and Netflix.

Tesla Q2 Earnings (Wed 19th)

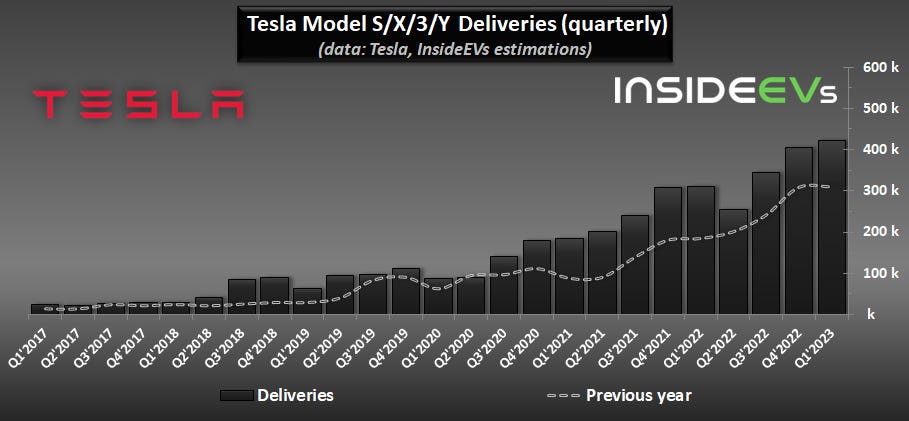

The EV giant has been in the news recently (when is it ever not) for two main reasons. Firstly, the production numbers, released ahead of earnings, came out. These were positive, the figures below including the YoY change:

Total deliveries Q2 2023: 466,140 (+83%)

Total production Q2 2023: 479,700 (+46%)

A longer term view of the growth is depicted well in the below delivery graphic:

The second element has been the price cuts that we’ve seen, used to boost demand. Musk has been outspoken in being happy to make less profit per car if it means that Tesla can be a volume car maker and grow market share that way.

The price cuts preceded the delivery figures, and do indicate that the reduction in price has increased demand. Yet the key element from the earnings figures will be to see whether the higher car sales has done enough to offset the reduced income per car.

Revenues for the quarter are expected at $24.69bn, YoY growth of 46%. This would match up to the change production. We therefore are optimistic that the price cuts have been offset and that financials in Q2 will be firm.

Add into the mix the $7,500 tax break credit for clients in the US and other perks in selected markets and we feel there’s enough momentum in the short term to keep the share price buoyed.

However, we are less bullish going into the end of the year. Cutting prices isn’t a long term strategy. It’ll undoubtedly put pressure on profit margins, which don’t really have much room to support this.

The current return on equity is very good at 28.70%, but if margins fall this will have a negative impact on this financial ratio too. Competitors such as BYD and Rivian are gaining pace and are also coming closer to taking more market share from Tesla.

CAN TESLA KEEP THE PARTY GOING: YES IN THE SHORT TERM, NO BY YEAR END.

Next up we turn to Netflix…

Netflix Q2 earnings (Wed 19th)

The Netflix share price has been on a tear over the last year. The disappointment in H1 2022 with the earnings and dampened sentiment did see the price come lower. Yet over a one-year period, the stock is up 157%.

Investors will be watching to see if this can continue next week with the Q2 earnings released. The key areas to watch for are the paid-sharing rollout and the advertising supported offerings.

Given the benchmark of expectations, it’s going to be tough for Netflix to materially surprise to the upside. We’ve seen several headlines like the below that indicate people are actively cutting back on memberships to services like Netflix.

Wall Street are forecasting a 12% fall YoY in earnings per share at $2.83. Revenue is due to come out flat at just over $8bn.

The other key element is subscriber growth. The forecast is for an addition of 1.8m subs for the quarter. As the chart below highlights, total subscriber growth is certainly slowing down, with it stagnant for much of last year.

We feel the consensus of 1.8m new subs is ambitious. Granted, this would match the figure from last quarter, but we believe there’s been more pressure on the subscriber base given high inflation and cost-of-living impact on consumers globally.

One point worth flagging is the commentary around the rollout of paid sharing. Not only should we get some in-depth data on the progress, but we’ll see how flexible the business is to either push forward or be flexible in changing this approach depending on how successful it has been in the trial markets.

CAN NETFLIX KEEP THE PARTY GOING: PROBABLY NOT

Ahead of the earnings next week, we’ll be releasing out top ten trade ideas as always on Monday. This includes five from the equity market, with charts and target levels.

Our latest piece (with many hitting TP levels this week) can be found here.

Good article

Hope so!!