Here at AP HQ, we’ve always put our money where our mouth is. However, before this year, we all traded and invested via different portfolios. Some of the feedback we received from early subscribers was that they’d like us to have a separate AlphaPicks Portfolio, whereby we invest in the thematic ideas that we write about and take advantage of opportunities that we flag up.

This seemed like a good idea, so we pooled some cash together and launched our portfolio as of Jan. 1st 2024.

To keep us honest, each month, we published a portfolio update to our paid subs, detailing what we bought and sold, along with our holdings at any point in time. Given we’re a multi-asset unconstrained fund, we set our benchmark as 40% equities / 30% fixed income / 20% commods / 10% FX (more details on the exact benchmark can be found in any of the updates).

Although we aren’t QUITE at the end of the year, we thought this would be a good time to look back. Instead of doing a dull market wrap, we wanted to run through some of the biggest themes of the year via our trades, outlining some of the best and worst trades as we navigated the year. As a note, these aren’t necessarily the positions we made or lost the most money on, but rather when our conviction calls or thinking was spot on (or terrible).

Enjoy!

Portfolio Return vs Benchmark

AP Port: +17.01%

Benchmark: +11.07%

Best Trades

Q1

Barclays Turnaround

Back in January, we wrote a piece entitled “Why Barclays Is A Screaming Value Buy”, which was quite a strong title. We spoke about the low P/E ratio, generous dividend yield and relative value metrics versus other banking peers. With the CEO due to release in February details of the transformation effort dubbed Project Minerva, we thought it was a good inclusion to buy.

Barclays rallied almost 26% in Q1 alone and has continued to do well, with us taking profits on the trade in the summer.

Coinbase

The team’s outlook on crypto was bullish as the year started, and we saw value in adding exposure to some of the related names. We bought Coinbase shares for around $125 in January and had doubled our money by the time we sold in late March.

It’s true that the stock now sits at $310, but we flag that it was trading sub $150 even in September, so we feel it was the right play to trim when we did. Arguably, the missed trick was going back in Q4, but we did add direct crypto exposure (more on that below).

Q2

Palo Alto Reversion

PANW was one of our largest portfolio holdings for Q2, with us being able to jump on the stock after the February drawdown and ride it back higher patiently:

However, with decent unrealised profit on a large holding, we spoke about what we wanted to do as we approached May earnings. In the end, we decided to simply cut half of the position and bank profits. We sold the rest later in the summer, but given the move higher in Q4, we should have left some money on the table. But this was still a great purchase post Feb earnings for a mean reversion.

Britvic Takeover

This was a great play that we jumped on in June. We wrote about it in detail just as we bought the stock in “The Takeover Tussle”. Carlsberg had made two takeover bids for Britvic within a month. These were both unsolicited but highlighted its strategic interest in expanding its presence in the soft drinks market.

After doing our own research, we felt that not only was a third bid coming, but an improved offer would likely get Britvic to say yes if it was closer to the 1,300p level. As a result, we bought the stock at 1,080p, were correct about the higher (and accepted) offer, and have enjoyed the ride higher.

Q3

China Pop

In late September, we wrote a piece called “China's Bazooka”, where we discussed the short-term potential for an equity market rally. In the conclusion we noted:

“We raise this to note that there are some big names who have taken the contrarian view on China and are looking for bigger rebounds in the market. Our take is that stimulus efforts can lead to some tactical trades in China, but we aren’t here for the long run.”

In terms of trade expressions, we liked Meituan and Alibaba but ended up going long the CSI 300 and Alibaba in the portfolio.

Both trades paid off handsomely, with us taking profits in early October. The percentage gains from both are shown below:

Q4

Bitcoin Breakout

Ahead of the US election, we published two pieces that led us to buy Bitcoin. The first was a Trump trade rec in our U.S. Election Trading Primer. Then, in late October, we released “Is A Bitcoin Breakout Coming?” where we flagged up factors such as the technical picture, our bias towards a Trump victory, investor flows and the cross-asset correlations.

We went long at $67k and benefitted from the rally that has since ensued. As we posted on X, we trimmed half of this ahead of $100k, with the other half being moved into ETH:

We’re not against going back in on BTC, but it’s a very volatile asset that we have to use very carefully within the portfolio to avoid large potential drawdowns or generally causing the portfolio to trade more like a meme stock than an investable fund.

Worst Trades

Q1

Snowflake Earnings

This was an incredibly frustrating one. We bought SNOW shares to start the year and were up circa 25% going into earnings in late Feb. Our mistake was not partially hedging our exposure here, but we didn’t expect such a volatile reaction in February. The CEO stepping down and a weaker-than-expected outlook saw the stock fall 20% overnight.

We held onto the position after this for longer than we should have, causing us to take a hit that really could have been avoided given that we had such a buffer room to set a stop at flat.

Boeing Blowout

Just a few weeks before we started the portfolio, we wrote a piece entitled “Boeing's Booming Orders And Bullish Momentum”. New orders and a host of analyst upgrades made the stock look attractive to us as a value play, much the same way as Barclays. So when the first issue of a door on a Boeing 737 MAX 9 aircraft blowing out and the stock fell, we thought this would be an isolated incident to which the market had overreacted.

As history now tells us, this was the start of multiple issues for Boeing planes, which caused scandals and a lot of headaches for Boeing investors.

Q3

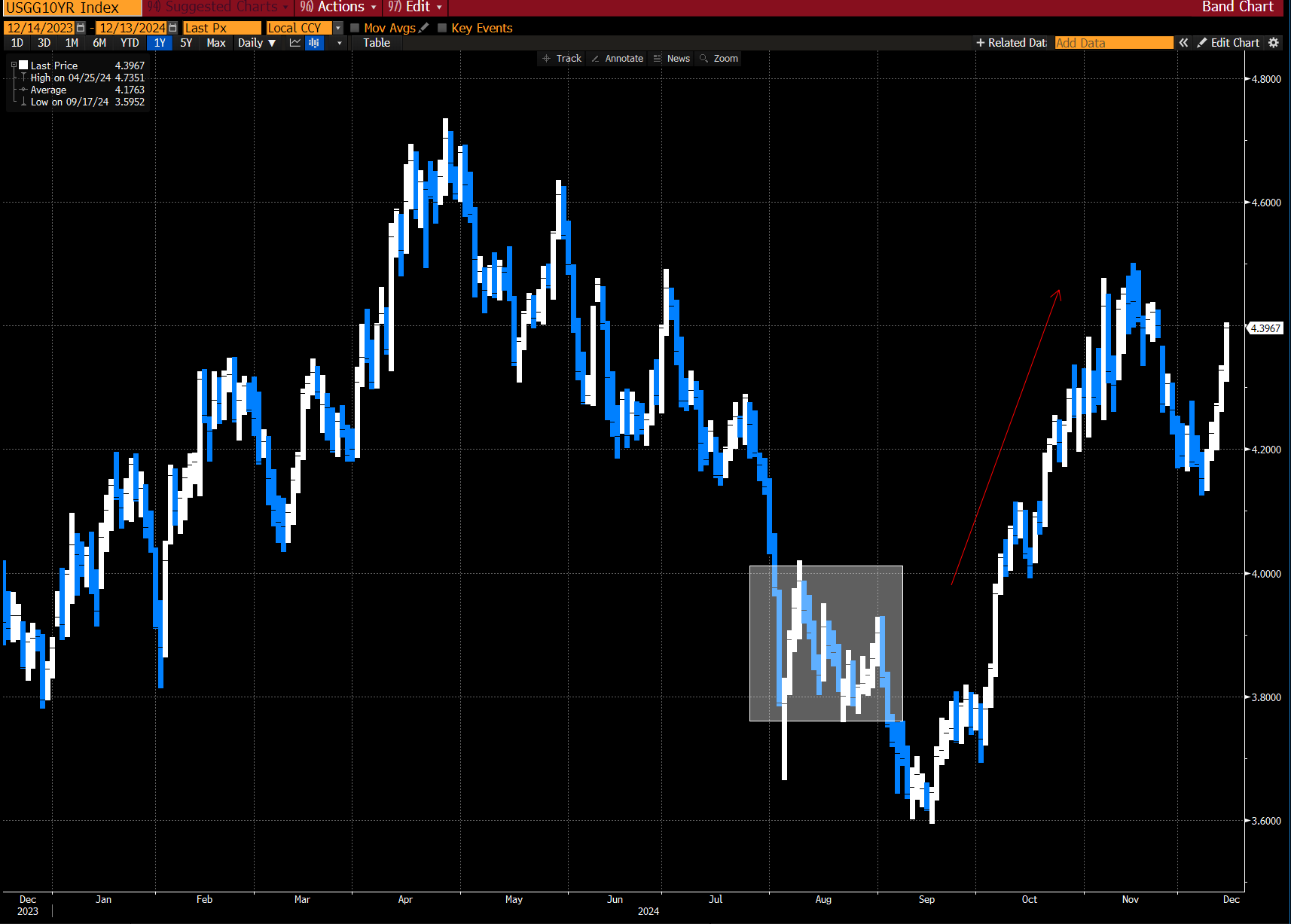

US Treasuries

Over August, we increased our exposure to bonds, moving into some UK Corp debt as well as US Treasuries in the 7-10-year space. We felt that, particularly in the US, the narrative of faster-than-priced Fed cuts would play out.

Even though we did see our Treasury positions initially move in our favour into September, bond yields went on a mega rally in Q4, fuelled by stronger US data and a market that was more risk-on than we had anticipated.

Q1-Q4

Not owning Nvidia

No explanation is needed.

Memedroid")

The Road Ahead

Our exposure in 2024 was heavier on equities than expected, but one simply had to be overweight US stocks, given the investor flows there this year.

As we close out the year, we definitely feel the bond markets are telling us something - namely that the Fed might have to cut back on rate cuts due to higher realised inflation. In fact, the existing rate cuts might already have started to fuel the inflation fire, and we haven’t even started on Trump’s fiscal spending agenda.

Geopolitics should play a heavy part next year, which will likely see us take more commodity exposure (we had it this year, just not focused on in this piece).

We were FX light and derivatives light, but this was mainly a function of our trading platform and margining requirements. We recently moved to Interactive Brokers, which looks like we’ll be able to solve this in 2025.

We hope you enjoyed this round-up. To stay in the loop in more real-time about our trading activity, consider becoming a paid subscriber to access our chat posts and monthly portfolio updates.