Tariff Trading: The State of Play

Takeaways from a manic week.

The volatile, whipsaw nature of global capital markets this week has been nothing short of incredible. The comparisons of the “highest/lowest level since X” start to fade into insignificance.

Rather than just looking at price levels and the relative moves to historical prices, understanding the drivers behind the moves and how to position and trade with conviction during these periods (even if conviction means sitting in cash) is more important.

As a quick disclaimer, we understand that newer readers might wonder with what authority we can be considered credible. For reference, our Global Asset Portfolio is down 1.05% Year To Date through 10th April, with the S&P 500 down 7.22% over the same period. The relative outperformance is based on some of the points below.

The bond bonanza

In late March, we wrote a piece entitled “Basis Trade Blowouts,” in which we discussed a recent academic paper entitled “Treasury market dysfunction and the role of the central bank” by Anil Kashyap, Jeremy Stein, Jonathan Wallen and Joshua Younger.

The paper discussed the fragility of the U.S. Treasury market and proposed strategies for the Federal Reserve to mitigate future disruptions. Part of any potential disruptions comes from hedge funds playing the basis trade, which ironically was a factor in this week’s severe dislocation in the Treasury space.

The violent increase in the 30-year SOFR swap spread can be seen below, with at least some of this coming from a rush for the exit from funds looking to close out existing basis trades:

You’ve had the deadly mix of Treasury yields spiking (so the collateral is worth less) and repo rates increasing (financing costs higher), meaning that unwinding has occurred, with the basis widening as futures have become rich with some flight-to-safety demand.

So far, the Fed hasn’t stepped in, but there is a precedent for them doing so, notably back in March 2020. Back then, it was estimated that the central bank bought $4 trillion of Treasuries and government-backed mortgage securities to stabilise the market.

The problem now is that the Treasury market has become much larger, even in just a few years. If the dislocation continues, the Fed will likely need significant money to sort this one out.

The question then is, by stepping in, are they providing the funds with a get-out-of-jail-free card? Moral hazard, blah blah.

From our perspective, we were close to needing intervention to have an orderly market, but Trump provided the backstop with his tariff pause yesterday. Although we didn’t get involved in basis trading, we did take on more bond exposure earlier this week.

In terms of specifics, we bought long-dated UK Gilts (30-year) under a similar premise that the central bank wouldn’t tolerate a further seismic shift (still getting over Liz Truss).

The other rates trade we added ties in with the next point…

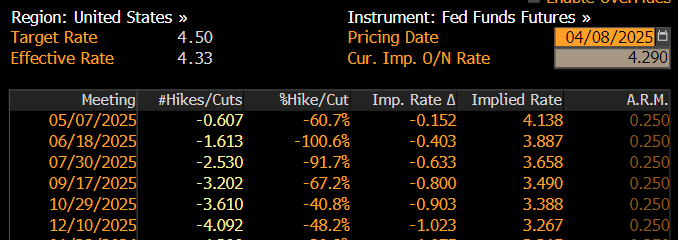

The rate-cut party doesn’t exist

On Tuesday, Fed funds futures were pricing in four rate cuts by year-end. During the day, this got close to five cuts. The growth scare was there, but we just didn’t feel like this was sane market thinking. The Fed have a mandate to control inflation, and tariffs would certainly pose a threat to the transitory commentary that Powell recently offered regarding the inflation outlook.

As a result, we shorted the Dec ‘25 SOFR futures at 96.70, looking for a move lower, which would reflect around two cuts this year.

This was more of a gut-feeling trade from the team, but the sharp reaction to Trump’s announcement helped to validate the conviction that emergency rate cuts won’t be needed. At the same time, this tactical trade doesn’t change our medium-term conviction of the yield curve steepening, but rather, we see the steepening being driven by a rise in both the short-end and the long-end of the curve. Yet the greater move in the long end is what should provide the curve gradient to increase.

Steepeners for tax cuts

One of the reasons why we have this view was expanded on with our musings on Wednesday in “Duration Has Left The Building.”

We feel Trump’s next stage after tariffs will involve taxes—extending TCJA, lowering corporate taxes from 21% to 15%, and eliminating taxes on social security benefits and tips.

If these tax cuts materialise without an offsetting fiscal contraction elsewhere (and let’s be honest, nobody is cutting entitlements), then we’re looking at the type of procyclical fiscal easing that invites term premium repricing. This is a bear steepener in every classic sense—front-end anchored by inertia, long end adjusting violently to the realisation that the Fed may have to do more just to keep pace with the inflationary impulse of fiscal expansion.

The tariff news from Wednesday doesn’t really change this theme. It might delay his moving to tax cuts slightly, but the fundamental view remains intact.

In terms of expressing this view, we’re holding off right now just for the dust to settle in the Treasury space, but we will likely add on exposure before the end of the month.

Option vol

Part of what has led our portfolio to outperform in recent weeks has been short-dated option exposure. More specifically, SPX Puts.