The Art of the Deal is LNG

Tariffs are the taxes of war. But not all wars are fought for conquest—some are fought for contracts.

As the tariff drum beats louder, the question echoes louder still: What is the endgame? Surely not chaos for its own sake. While tariffs would bring in revenues, the knock-on effects of the current approach (escalated tensions with nations worldwide) would also hurt the U.S., reversing any positives it may create. But perhaps this isn’t madness but rather manoeuvre. Not protectionism as an ideology but as an instrument. A gambit, not a doctrine.

Washington knows the world doesn’t hunger for its denim or whiskey. American cars don’t turn heads in foreign streets. And while Silicon Valley still sits atop the digital throne, tech dominance is already a known quantity—it doesn’t need a trade deal. What remains is fire and fuel. Beneath American soil lies the one asset every industrialising nation wants: Energy.

And so, the strategy unfolds. Tariffs are not the destination; they are the toll booth on the road to energy diplomacy.

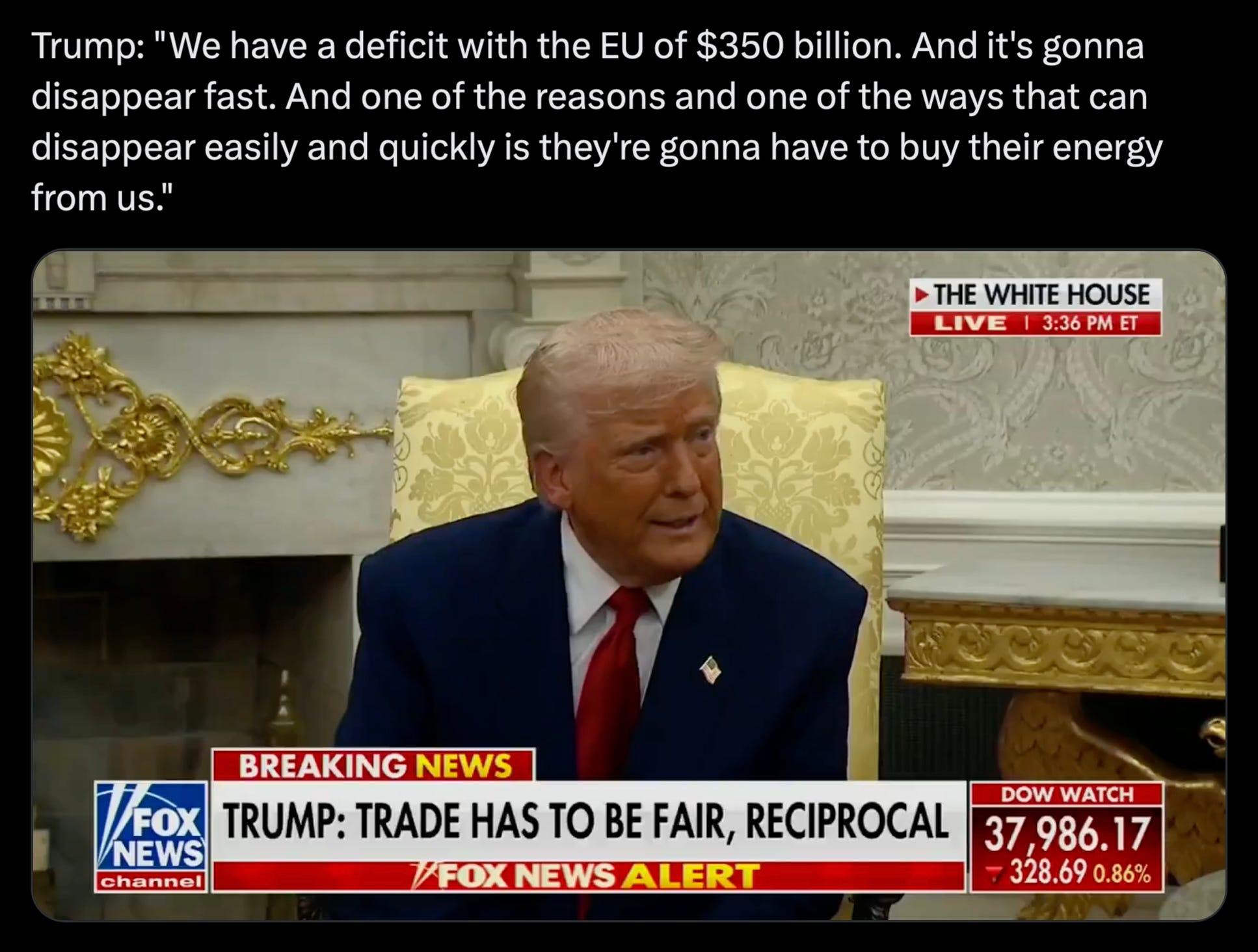

“They’re gonna have to buy”

In 2018, Trump famously said, “Trade wars are good, and easy to win.” At the time, markets laughed—or at least pretended to. They’re not laughing now.

On Sunday, Trump made clear that energy would be the lever to narrow the trade deficit with Europe. He didn’t frame it as a mutual need or shared benefit. He said plainly: “They’re gonna have to buy.” Less of a negotiation, more of a directive.

Behind that bravado may be some structural truth. Roughly one-third of its energy consumption still comes from oil. Before the Ukraine war, Russia provided 30% of those imports. That number has collapsed to ~10% under sanctions, with the gap now filled by Norway, the U.S., and the Gulf states.

NatGas tells the same story with sharper lines. Russia once accounted for 40% of EU gas imports. By 2024, that’s below 10%. Norway has stepped in via pipeline (25–30%), but the real swing player is the United States. American LNG now supplies 20–25% of Europe’s gas (up from almost zero a decade ago), making it Europe’s top LNG provider. Qatar remains relevant at ~15%, but the growth trajectory belongs to the U.S.

Today’s note isn’t about energy in the broad sense. It’s about LNG—the liquid weapon of this new economic doctrine. We flagged the setup in March (“America’s LNG Boom Reshapes Global Energy”), and recent developments have only reinforced that view. In a world of fiscal erosion, tariff escalation, and fractured alliances, LNG exporters sit in the eye of the storm—and they look like they may emerge as out-performers.

Already in the newsfeed

An extract from our article on March 12th, 2025:

“Advancements in horizontal drilling and hydraulic fracturing unlocked vast reserves, from the Permian Basin to the Marcellus Shale, unlocking previously inaccessible oil and gas reserves. Production soared, surpassing 100 billion cubic feet per day. Today, natural gas fuels 41% of America’s power grid, outpacing coal and nuclear. More importantly, it far exceeds domestic demand—meaning exports are the name of the game.”

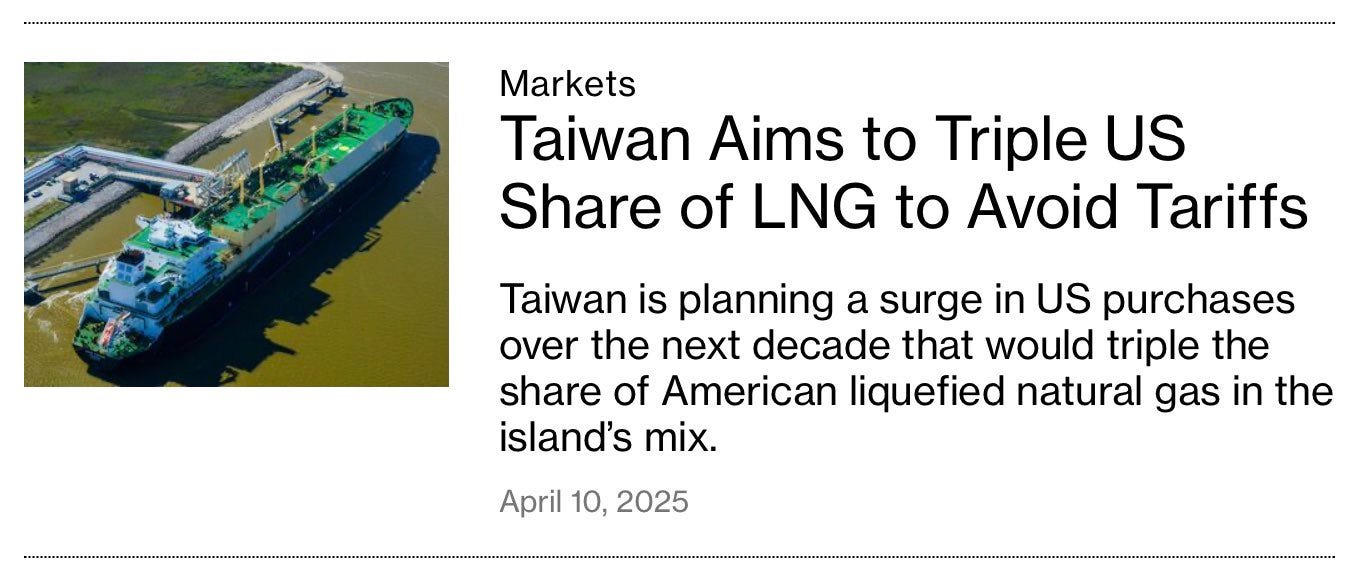

Two weeks on from the Liberation Day tariffs, the first tactical adjustment has already landed: a 90-day pause on the levies. On the surface, it may read as a market-soothing gesture (call it the “Trump Put,” if you like). While that may be true, this isn’t about calming markets. It’s about creating pressure. Time is now the leverage.

We’re not here to play Bill Ackman on X, cheerleading every pivot like it’s a policy breakthrough. The reality is simpler: major economies—Europe in particular—don’t move under deadline. Their size and complexity make quick concessions structurally impossible. But emerging markets? That’s different. Smaller nations can’t absorb uncertainty in the same way. For them, 90 days is an ultimatum.

Not every country has the luxury of waiting. We expect deals to start landing well before the deadline, initially with EMs, then scaling up in size and scope towards larger economies, likely after the 90-day extension for major players, though.

And the signalling has already begun.

Last week, Scott Bessent spoke with CNBC. The Treasury chief reiterated that Trump would be directly involved in the talks and suggested that the nature of the agreements would be something different than standard trade deals that focus on bringing down barriers to commerce—incorporating an energy project, for example.

“So, what’s the play?”

LNG Exporters

U.S. LNG exporters are entering a golden era fueled by geopolitics, tariff threats, and global demand from Europe to Asia. As Trump uses energy diplomacy to shrink the trade deficit, quality LNG names are the real winners… Upstream, midstream, and especially the shippers.

Trump’s latest move to bend global trade in America’s favour? Simple: tariffs as the stick, LNG as the carrot.

Start upstream: EQT Corp (EQT) and Antero Resources (AR) are sitting on massive Marcellus shale gas reserves (more than the U.S. can consume).

Midstream? Cheniere Energy (LNG) is the bellwether, with Sabine Pass and Corpus Christi terminals already running full tilt. They’re turning domestic oversupply into global opportunity.

But don’t sleep on the unsung heroes: the shippers. Companies like Flex LNG (FLNG) and Golar LNG (GLNG) operate the tankers hauling this liquefied gas across oceans. As demand spikes, so do charter rates. When countries start panic-buying to stay on Trump’s good side, these vessels become floating cash machines.

Trading NatGas futures is like wrestling a greased pig. It’s called the “Widow Maker” for a reason. Weather-driven, twitchy, and maddeningly volatile. I’ve traded (and made markets) on Henry Hub (ICE and CME). Trust me, there are easier ways to lose your sanity.

But LNG stocks? That’s the smart way to ride this macro wave. You get leveraged exposure to a secular trend without the ulcer. These companies are the picks and shovels in America’s energy push… Scalable, steady, and built to profit from policy shifts.

Skip the NYMEX rollercoaster. Go long the names turning America’s gas glut into global leverage. With Trump lighting a geopolitical fire under LNG demand, these companies aren’t just riding the storm; they are the storm.

Watch them. Own them. Ride the wave.

The LNG exporter basket

The thesis is in. More importantly, how are we allocating? A short breakdown of the ten names we’re adding to a new LNG thematic basket can be found below.

Cheniere Energy (LNG) – Terminal

The heavyweight of U.S. LNG exports. Owns and operates Sabine Pass and Corpus Christi terminals—infrastructure that already dominates outbound U.S. LNG volumes. This is the benchmark name in the LNG trade.

Sempra (SRE) – Terminal / Utility

California-based utility giant with a growing LNG footprint via its controlling stake in Sempra Infrastructure, which owns the Cameron LNG facility and is expanding aggressively in North America.

Antero Resources (AR) – Upstream

An Appalachian E&P player with direct exposure to liquids-rich gas production. Strong link to LNG feedstock flows and one of the more aggressive names in terms of volume growth.

National Fuel Gas Co. (NFG) – Integrated / Midstream

A vertically integrated gas player with upstream and midstream operations in the Marcellus. Provides indirect leverage to LNG via feedstock production and transport infrastructure.

Spire Inc. (SR) – Utility / Midstream

Regional gas utility with long-haul pipeline exposure. A slower-moving name, but positioned to benefit from any ramp-up in domestic gas demand due to exports.

EQT Corp (EQT) – Upstream

The largest natural gas producer in the U.S. Well hedged, low-cost operator supplying major LNG terminals. A pure upstream bet with deep LNG sensitivity.

NextDecade Corp (NEXT) – Terminal / Development

Pure-play LNG growth story. Still pre-revenue, but its Rio Grande LNG project has seen real momentum. This is the optionality bet if U.S. LNG demand structurally accelerates.

Golar LNG (GLNG) – FLNG / Shipping

Floating LNG (FLNG) pioneer. Owns and operates liquefaction vessels — a strategic asset in flexible, fast-deploy LNG solutions. More global but still exposed to U.S. trends.

Flex LNG Ltd. (FLNG) – Shipping

Specialised LNG shipper with a modern fleet of carriers. High spot rate sensitivity and direct exposure to LNG volumes — plays the transport angle in the global LNG trade.

Stabilis Solutions (SLNG) – Small-Scale LNG

Micro-cap name in small-scale LNG production and distribution. Niche, but could benefit from policy tailwinds aimed at regional or remote LNG adoption.

The names are sorted by what we are allocating the most weight to. Specific weights in our basket can be found below.

We’re starting by allocating about 400bps in the portfolio to this basket. Our cash holdings have been high throughout this market turmoil. While we do not think the end is near for elevated volatility, we’re happy to put some risk on this thesis, given that headlines are already hitting, which may provide some tailwinds to the industry.

As always, trade safe. There will be plenty more themes to come out of these global shifts, along with many more macro updates and trades along the way.

AP + PiQ

| A guest post by

|

💪💪

no value plays in this area? Antero, RRC, EQT insiders have been sellins shares in the last months.