A combo of a divided Fed, yentervention, and higher oil can’t derail the equity train right now, with earnings as the driver.

The S&P 500 notched a fifth consecutive weekly gain, grinding to fresh record highs as month-end flows and a late-week risk bid helped offset what was otherwise a choppy, headline-driven stretch. Friday’s push higher, driven by institutional rebalancing and renewed optimism around US-Iran negotiations, masked a more uneven tone beneath the surface, where dispersion across sectors and within mega-cap tech continues to define the market.

AI beneficiaries once again led from the front. Strength across semiconductors remained the clearest expression of the current macro regime (“chips as macro”). The latest round of mega-cap earnings highlighted a more nuanced reality. Alphabet (GOOGL US) and Amazon (AMZN US) were rewarded for tangible progress, while Meta Platforms (META US) and Microsoft (MSFT US) were punished for leaning further into spending without yet delivering a commensurate payoff.

Outside of tech, leadership broadened modestly. Caterpillar (CAT US) provided a reminder that the AI buildout extends beyond silicon, with power and construction demand feeding into industrial upside. Energy also continued to grind higher as geopolitical tensions lingered, even as the market has grown more accustomed to trading around the Iran conflict rather than through it.

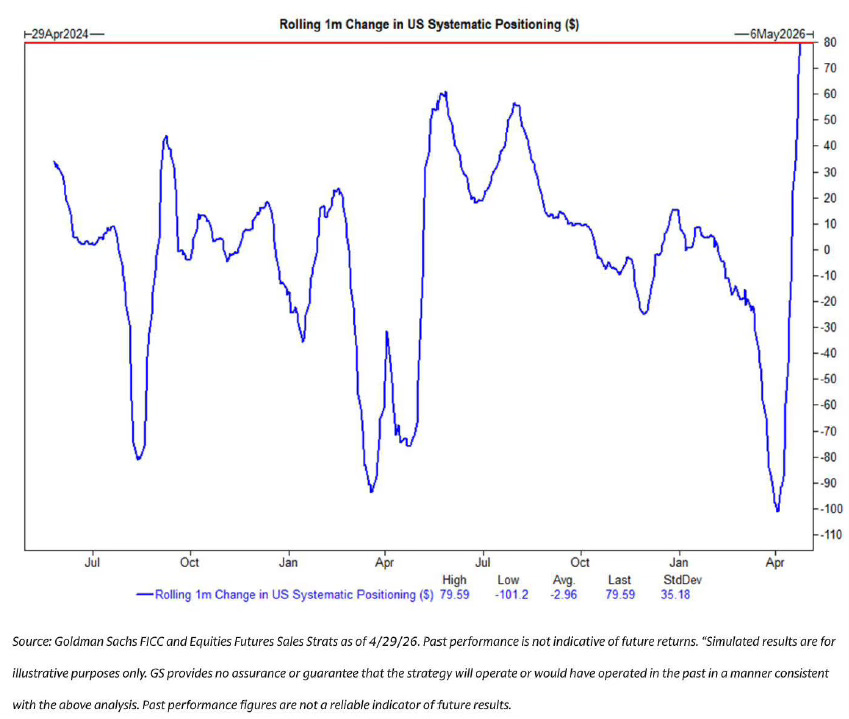

Under the surface, however, the setup is becoming more technical. With month-end rebalancing behind us, attention shifts to systematic flows, where Goldman Sachs flags CTAs as potential sellers across scenarios in the week ahead. That introduces a degree of fragility to what has been a flow-driven advance, particularly given how much of the recent strength has come from positioning resets rather than fresh fundamental conviction.

“The one-month change in US positioning across the major systematic cohorts is the 2nd largest re-leveraging in our dataset going back to 2016. Systematics have bought almost $80 billion of US equities in the past month, and CTAs are now long $44 billion of US equities.”

Macro signals remain broadly supportive, but not emphatically so. The Federal Reserve delivered a hold as expected, though the presence of multiple hawkish dissents complicates the path forward for policy under incoming leadership. Growth data continues to show resilience, particularly in business investment and consumption, but the mix is not clean enough to shift the policy narrative decisively. Markets briefly reverted to a more textbook reaction function on softer ISM data, suggesting that the distortion from geopolitical noise may be fading at the margin.

In rates, the tone was more cautious. Treasury yields edged higher following the FOMC, with the long end approaching key technical levels that could act as a volatility trigger into May. In FX, dollar weakness was more about external shocks, most notably intervention in USD/JPY and a hawkish tilt from the ECB.

That all results in an equity market that continues to move higher, but with a shifting burden of proof. AI remains the anchor, flows remain the accelerant, and geopolitics remains the wild card. The trend is intact, but the composition of the rally (narrower leadership, greater sensitivity to earnings quality, and growing reliance on technical support) suggests that the next leg higher will require more than just momentum.

Let’s get into the guide to trades moving markets, where things stand and where they may be heading.

“Software and Private Credit”

“The Market Chooses Its Own Adventure”

“Yentervention”

“A Broken Cartel”

Software and Private Credit

For much of the last six months or so, private credit has traded as a software derivative. Private credit funds lent heavily to software businesses during the last cycle, and the market has spent this year marking down anything that looks vulnerable to AI substitution, lower seat growth, or weaker pricing power. Last week brought the first real shift to that narrative.

Ares (ARES US), Blackstone (BX US), and Blue Owl (OWL US) all moved to reassure investors last week on software exposure, with scorecards, outside consultants, and portfolio reviews designed to separate actual AI vulnerability from market panic. Blackstone’s BCRED said less than 5% of investments faced AI headwinds, Ares said 85% of its software-oriented investments were low risk, and Blue Owl reportedly found “minimal” risk after re-underwriting loans for AI vulnerability.

There is an obvious “talking your own book” element here. That is not a criticism of them. Private credit is built on confidence, marks, funding access, and the continued belief that senior secured exposure can survive equity volatility. Nobody in this ecosystem has an incentive to declare the collateral impaired before the cash flows force the conversation. The question is, however, whether the next refinancing cycle agrees with their scorecards.

The other narrative shift came from software itself. Atlassian (TEAM US) was the cleanest expression last week. TEAM surged after earnings, with revenue and adjusted earnings ahead of expectations, cloud revenue growth of 29%, and management leaning hard into the idea that AI is a product accelerant rather than a terminal threat. After months in which “AI risk” was enough to flatten almost anything with recurring revenue, the market is finally rewarding a software company for showing resilience and a path toward profitable growth.

Don’t get us wrong, this one shift does not kill the software bear thesis, but we will see a more selective market approach to software going forward.

For markets, that is the important transition. The first phase of the trade was indiscriminate. Software was sold first and analysed later. Private credit firms with perceived exposure were dragged into the same bucket. The next phase should be more dispersion-led. Some software companies will show that AI improves distribution, workflow depth, and customer value. Others will discover that AI compresses pricing, reduces seats, weakens moats, or gives customers a credible reason to renegotiate.

Our read is that last week marked a shift from panic to underwriting. That is constructive for the best software names and the cleaner private credit platforms, but it does not remove the fault line. That is where we think the market will spend the next few months. Not in a broad private credit collapse, and not in a full exoneration of the asset class either. More likely, we get a slow separation between managers that can prove genuine insulation and those that merely disclose it.

The indiscriminate short-software / short-private-credit trade has probably lost its momentum, and the easy leg is behind us. The software names that can show AI-enhanced demand, stronger retention, and improving profitability will outperform, especially out of oversold conditions.

In case you missed it, we released our latest primer over the weekend mapping private credit and the software risks.

The Market Chooses Its Own Adventure

US equities pushed to fresh highs and capped their best month since 2020, even as the Fed delivered a more divided message and Japan stepped back into the yen market. In another regime, either of those stories would have been enough to cause headaches. A fractured Fed path would have been the rates story. Yen intervention would have been the global macro story. Instead, both were treated as supporting characters, all to the leading role which still belongs to AI.